Forest Products Industry Lookahead

Author: Caleb Fetner

The last few years have brought a lot of change to the forest products industry. Companies have bought, sold, and closed facilities and a new company, Global Cellulose Fibers, was formed as International Paper made strategic shifts. Several states are focused on extended producer responsibility (EPR) laws for packaging, which could favor paper-based packaging over plastic, but also creates a regulatory patchwork when different states have different requirements. While companies have sustainability goals, we haven’t really seen a large carbon reduction project in the pulp and paper industry yet, and this is certainly not a priority for the current administration. In the wood building products space, we hope for lower mortgage rates in 2026 to spur the demand for new homes. With the current deregulatory atmosphere and push for permit streamlining, 2026 could be the year to plan and permit capital improvements to optimize production and energy efficiency and reduce operating costs.

The forest products industry is fairly heavily regulated from an environmental standpoint. Although the general trend at the United States Environmental Protection Agency (U.S. EPA) is deregulation, there are some things to watch for in air quality regulations. We will see a revision to the National Emission Standards for Hazardous Air Pollutants (NESHAP) for Plywood and Composite Wood Products (PCWP MACT) this summer. The revised rule will fill gaps and address hazardous air pollutant (HAP) emissions from all sources at lumber, plywood, and composite wood products mills. Facilities will have first-time work practice requirements for lumber kilns and resinated material handling operations and additional emissions limits on dryers and presses. Look for an industry workshop hosted by the American Wood Council (AWC) and the National Council for Air and Stream Improvement (NCASI) for a deep dive into the new requirements and how to comply. The pulp and paper industry was originally expecting to be working on completing an information collection request from U.S. EPA this year to inform its technology review and gap filling for 40 CFR Part 63, Subparts S and MM, and 40 CFR Part 60, Subpart BBa, but the current administration will not issue an information collection request (ICR). Instead, some companies have volunteered to collect information that would inform the regulatory review and allow the current administration to develop proposed rules.

U.S. EPA also needs to make revisions to the Industrial Boiler NESHAP based on a court ruling related to the new source standards, so forest products facilities should also be tracking that closely. Reopening the rule is also an opportunity to make clarifications around compliance procedures for multi-fuel boilers that are common in the pulp and paper industry. Speaking of pulp and paper mill boilers, U.S. EPA is also expected to propose changes to the Good Neighbor Plan (GNP) that established first-time nitrogen oxides (NOX) emissions limits for fossil fuel boilers at paper mills in certain states. That rule is currently stayed, and we hope that U.S. EPA’s upcoming actions to approve ozone transport state implementation plans (SIP) that were previously rejected and resulted in the need for the GNP means that an updated analysis will show that NOX emissions reductions from paper mill boilers are not needed to achieve attainment with the 2015 ozone standard in downwind states. We are also hoping to evaluate less forest products mill sources for emissions reductions under the Regional Haze Rule with the expected changes that should be proposed in 2026 ahead of the next planning period, at least in areas that have already made significant improvements in visibility. Our air quality lookahead article details other cross-cutting air-related issues to watch for in 2026.

On the Toxics Substances Control Act (TSCA) front, the industry is watching the recent proposal related to U.S. EPA’s risk evaluation for formaldehyde. U.S. EPA’s revised approach would mean the removal of the unreasonable risk determination for inhalation exposure to formaldehyde by wood products manufacturing facility workers. See our recent article for more information. If U.S. EPA finalizes the revisions as proposed, wood products mills would not be subject to additional formaldehyde inhalation risk management rules.

In the world of water, we expect potential changes to the Clean Water Act (CWA) Hazardous Substances Facility Response Plan (FRP) rule to be impactful to the forest products industry. As discussed in our water lookahead article, measures to delay compliance dates and make changes to the rule have completed White House Office of Management and Budget (OMB) inter-agency review. We are expecting the delay to be up to five years and are hearing that U.S. EPA may consider increasing threshold quantities by 10 times, which could impact what facilities are subject to the rule and how many chemicals subjected facilities must consider.

For forest products facilities that provide drinking water to their employees and/or the outside community, ALL4 is tracking the American Waterworks Association’s (AWW) case against the October 2024 Lead and Copper Rule Improvements (LCRI). LCRI currently has compliance dates beginning in 2027 with later dates for lead service line (LSL) replacement. U.S. EPA has also proposed perchlorate drinking water standards, and on January 22 released a plan to develop a revised toxicity assessment for fluoride in drinking water. A D.C. circuit court has also blocked, for the time being, U.S. EPA’s attempt to roll back four of the six per- and polyfluoroalkyl substances (PFAS) maximum contaminant levels (MCLs) that were promulgated in 2024. We have a separate lookahead article dedicated to PFAS, which discusses a few other items with potential impact to the forest products industry including biosolids, Toxics Release Inventory (TRI) reporting, Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), one-time reporting under TSCA, and state-specific consumer product restrictions.

Many forest products facilities have stormwater discharges that are permitted under general stormwater permits – U.S. EPA’s Multisector General Permit (MSGP) is set to expire at the end of February 2026; we saw a draft permit in late 2024 (see our previous article) with extended public comment period until May 2025 but no movement since then. Though U.S. EPA’s MSGP only directly applies to facilities in a few states and other areas under U.S. EPA’s authority, many states adopt updates in U.S. EPA’s MSGP as they renew their own state permits. We are currently tracking state MSGP renewals in several states including Alaska, Wisconsin, Mississippi, Oregon, Texas, Kansas, and Louisiana.

On the energy and modernization side of things, aside from the air permitting and modeling regulatory and policy improvements we are hoping for, it will be interesting to see if there is an uptick in utilization of U.S. Forest Service grant programs like the Community Wood Grant Program. This program provides funding for grants to install thermal wood energy systems or build innovative wood product manufacturing facilities. The various programs support innovation, expand wood energy markets, and promote wood as a sustainable building material. Could we see a data center get energy from wood residuals under this program? At a minimum, these grants could help wood products facilities modernize their systems and optimize production.

The forest products sector is a core part of ALL4’s business and we have experts who have not only completed projects for mills as consultants but have also worked at mills and for regulatory agencies. Through staff shortages over the past several years, we’ve also provided extension services at a number of paper mills to bridge the gap until replacement staff can be hired and/or existing staff can be trained. When facilities have made the unfortunate decision to close, we have supported facilities in navigating permitting obligations through shutdown and/or transitional operations. Our staff brings a deep expertise to environmental, safety, and digital solutions projects for forest products clients. We are committed to helping forest products companies navigate environmental and health and safety policies and regulations, develop project strategies, and stay ahead of regulatory changes. If you have questions on how to navigate what’s ahead in 2026, please reach out to Lizzie Smith or Amy Marshall.

Data Centers 2026 Look Ahead

Author: Sharon Sadler

The data center industry is a rapidly growing sector in the United States with record-high private equity involvement and new companies entering the market. Data centers are increasing in both number and capacity to meet growing global connectivity, and as demand rises, so do some of the challenges the industry faces.

In our Data Center segment of Look Ahead 2025, we described how data centers play a critical role in supporting the global economy and must maintain uninterrupted, 24/7 operations to ensure reliability and performance. To achieve this level of continuous functionality, reliable access to electrical power, high-capacity fiber optic connectivity, and effective cooling infrastructure are essential foundational requirements. In addition, provisions for on-site power generation serve as a vital contingency measure, particularly in scenarios where utility grid capacity or readiness is insufficient or delayed.

With the increase in data center size and the potential for on-site generation, community impacts such as the environment and natural resources, noise, and viewshed become significantly more pronounced and warrant greater attention. Data centers work hard to reduce impacts by following the applicable federal, state, and local processes and regulations; employing reputable companies to design, build, and operate; mitigating noise where possible; maximizing water efficiency and other resource use; minimizing the impact to viewshed; training to reduce potential environmental impacts during operation; and building strong relationships with the area as good community stewards.

This Look Ahead 2026 highlights changes and trends we’re seeing in air regulations, the data center sector’s intersection with the power sector, and other topics of interest.

Changes in Air Regulations

Air quality strategy and permitting is important for data centers, and it is a changing landscape to monitor. Below are some examples from 2025 and what could play out in 2026:

Attainment Status: Whether a data center is in an attainment area or a nonattainment area significantly impacts air permitting. Because attainment status is evaluated at established intervals, it changes. Over the last several years, key data center locations have been redesignated as nonattainment or reclassified to a higher nonattainment status, resulting in more stringent air quality requirements in these areas. These changes require data centers to evaluate their existing campuses to determine whether they want to become a major source or establish a strategy through air pollutant controls or reduced operational flexibility to decrease potential emissions and avoid being a major source. Such changes also impact proposed builds and expansions with lower thresholds that trigger Federal construction permitting. A few examples:

- Redesignation to serious nonattainment for Maricopa County, AZ has been expected for years; data centers permitted in the region have intentionally and proactively accepted a potential emissions threshold of less than 50 tons per year (tpy) of nitrogen oxides (NOX) rather than 100 tpy NOX given the anticipated reduction of the major source threshold to 50 tpy NOX. On November 19, 2025, however, the United States Environmental Protection Agency (U.S. EPA) proposed a rule allowing the exclusion of international emissions from the area’s attainment status determination (the area would have attained the 2015 ozone standard by the required date but for international emissions). If this rule is finalized as proposed, Maricopa will remain a moderate nonattainment area with a major source threshold of 100 tpy NOX.

- The Dallas/Fort Worth (DFW), TX area has been redesignated twice in three years, reducing the major source threshold from 100 tpy of NOX to its current 25 tpy NOX. The next milestone date to evaluate attainment status is 2027 but if the abovementioned proposed rule regarding Maricopa County is finalized, areas relatively near U.S. borders that could potentially be impacted by international emissions may be revisited to determine if they would be in attainment in the absence of these emissions.

- The Greater Chicago, IL area was redesignated in January 2025 to serious nonattainment, lowering the major source threshold from 100 tpy NOX to 50 tpy NOX.

Hourly Emissions Rates: Short-term emissions standards contained in applicable Federal rules (e.g., Federal engine and turbine rules) have also been adopted by many state or local environmental agencies; compliance with the Federal standards is also sufficient for their programs (e.g., U.S. Tier 2- or Tier 3-certified, engine size dependent, for emergency generators). However, these agencies are also able to establish their own short-term (hourly) emissions requirements, often referred to as Best Available Control Technology (BACT) or similar, and they can be more stringent than Federal rules. These are also subject to change, so data centers must monitor state and local regulatory activity to ensure they procure the appropriate equipment. Below are recent examples where state-specific hourly emissions rates may change or have changed:

- Virginia established its current presumptive BACT requirements for diesel-fired emergency and non-emergency generators in 2012. While multiple pollutants are addressed, the most impactful pollutant is NOX, as it is the pollutant of greatest concern from diesel engines. The Virginia Department of Environmental Quality (VADEQ) established a 6.0 grams/horsepower-hour (g/hp-hr) NOX emissions rate for emergency generators and a 0.6 g/hp-hr NOX emissions rate for non-emergency generators. However, in late December 2025, VADEQ drafted updated presumptive BACT guidance that would require 0.6 g/hp-hr NOX for future diesel-fired emergency and non-emergency generators specifically at data centers, along with lower limits for other pollutants. This draft guidance would require emergency generators to meet U.S. EPA Tier 4 equivalent emissions standards. This draft guidance has not yet been released for public comment, which is the next step, and no timeline for its release is available.

- As of January 8, 2026, Illinois will require many new diesel-fired emergency generators at data centers to meet U.S. EPA Tier 4 emissions standards. There is also a more stringent emissions requirement for new natural gas-fired engines. For facilities that require Federally Enforceable State Operating Permits (synthetic minor) or Clean Air Act Permit Program permits, which are common for data centers in IL, the Tier 4 requirements begin with air permit applications for new data center emergency generators submitted beginning December 1, 2026.

Turbine Rules: U.S. EPA revised the Federal rules for combustion turbines, Standards of Performance for New Stationary Sources (NSPS) Subparts GG for pre-2005 turbines and KKKK for post-2005 turbines, in January 2026. NSPS Subpart KKKKa was added for turbines constructed, modified, or reconstructed after December 13, 2024, which will be the most applicable to data centers as interest in on-site generation increases. NSPS Subpart KKKKa establishes new subcategories of NOX emissions standards for different turbines based on size, utilization, and design efficiency. Among other changes, the creation of a subcategory for temporary small turbines is of particular interest.

- According to the Rule preamble, the creation of this subcategory was an attempt to better align the NSPS for other equipment such as boilers and engines that serve a facility for a short time. NSPS Subpart KKKKa establishes this new subcategory for temporary turbines, up to 850 MMBtu/hr, used in a single location for up to 24 months, meeting certain NOX The rule does not exempt these turbines but allows a streamlined compliance approach.

- The rule requires strict adherence to the 24-month limitation; there is no countdown reset if the unit relocates on property or another temporary turbine replaces the first, as long as the units continue performing the same function for the same site. If the unit remains on-site longer, U.S. EPA will retroactively apply the requirements of the rule as if the unit is now permanent, but beginning Day 1, which would likely result in noncompliance.

The establishment of this subcategory will benefit data centers looking to use subject turbines for less than 24 months to provide bridging power by reducing the compliance burden under the rule as compared to a permanent on-site power installation. However, each scenario will need to be reviewed with the state or local environmental agency as they may still require the turbine to be permitted; notably, U.S. EPA’s more general definition for temporary sources requires the unit to be on-site for no longer than 12 months and most states have adopted a similar interpretation. Prime power or non-emergency combustion sources may require an air permit by a state/local agency even if on-site for less than 12 months.

Power

Speaking of turbines, 2025 is known as the year of power, a moniker that will probably be assigned to each subsequent year for quite some time. There is dynamic discussion about power – how to generate and transmit enough, and who is going to pay for the expanded infrastructure necessary to meet demand, among other questions.

- Rates: Utility customers are worried about their electricity rates. In January 2026, the White House called upon data centers to shoulder the additional costs associated with the increase in energy production and transmission needed to serve the industry, and/or generate the power themselves. Some data centers have already issued statements that they plan to cover or offset a large portion of these costs to protect residents’ bills.

- On-site Generation: Developers and data centers are requesting on-site generation air permitting evaluations for a variety of sites. They need to understand how best to permit a combination of emergency generators and on-site generation equipment as site needs change. The balance is important ─ the need for power to bring buildings online but also the need to ensure that the underlying assumptions of the regulatory strategy (e.g., what data will be available from the engine and emissions controls if needed) can be achieved in a compliant manner during operations. There is also the question of source aggregation to consider – what needs to be true for the emissions from prime power generation and backup power generation to be considered separate, each with their own maximum allowable emissions threshold before Federal major source construction permitting kicks in.

- Emergency Demand Response: Data centers face mounting pressure to participate in utility programs using existing emergency generators to secure future power commitments. Programs such as emergency demand response to make use of emergency generators to stabilize the grid are not new, but the data center industry is engaging more than ever before to secure its place in the power queue. In the last year, with the power challenge top of mind and the White House prioritizing the U.S.’s lead in artificial intelligence (AI), there is hope across the data center industry that U.S. EPA could loosen its interpretation on how an emergency generator is allowed to operate if it complies with U.S. EPA Tier 4 emissions standards. U.S. EPA issued a May 2025 reply to Duke Energy’s request for concurrence that their PowerShare Mandatory 50 program met the five criteria for financial arrangement. However, this did not change how U.S. EPA interprets its regulations; it simply reminded the regulated community that such programs meeting U.S. EPA’s financial arrangement criteria exist. As of this article’s writing, U.S. EPA has not made a change to its interpretation; the 50 hours per year limit on non-emergency is still in effect, and the five criteria established by U.S. EPA to determine allowable financial arrangement operation for emergency generators still stand. That said, on January 20, 2025, U.S. EPA and the Data Center Coalition met “to discuss how the rapid growth of data centers can be harnessed to make the U.S. the AI capital of the world while keeping energy prices low and ensuring clean air, land, and water for all Americans.” The outcomes from the roundtable are yet to be determined but just days later, the Department of Energy issued a letter to utility grid Reliability Coordinators and Balancing Authorities in preparation for the January 24-25th winter storm. The Department was prepared to issue, and has since issued, several 202(c) orders as needed and approved to “ensure that the tens of gigawatts of available backup generation, which would otherwise stand idle, is available during emergency conditions,” authorizing Coordinators/Authorities “to direct backup generation facilities to run as a last resort before declaring Energy Emergency Alert 3”. Such operation is expected to be considered emergency and if operation results in a permit exceedance, those could be waived. The White House stated in a call before the weekend that a 202(c) order will protect facilities from environmental exceedances.

- Nuclear: Every power conversation weaves through renewable sources and low carbon fuels, and inevitably lands again on nuclear. For the last 18 months, the nuclear power discussion has reached a new level. There are varied opinions on whether the Three Mile Island nuclear plant will ever be recommissioned, as announced by Microsoft in Fall 2024, but it is acknowledged as a bold step for power. Small modular reactors (SMR) are viewed as the ideal power source for the 2030s and several entities are taking steps towards this goal. Dominion Energy and Amazon announced a plan in the fall of 2024 to team up to advance SMR technology at Dominion’s North Anna Power Station in Louisa County, VA, an existing nuclear power plant two hours south of ALL4’s own WDC office.

What Else?

In addition to changing air regulations and the hot topic of power, data centers are navigating additional challenges such as zoning changes, sophisticated and vocal public interest, and new water requirements.

- Zoning: With the significant increase in data center construction, data centers are frequently requesting counties (or other localities) change a zoning designation or re-zone a plot of land to allow the facility to be built. There is often an opportunity for the public to provide input on whether land is re-zoned, and it’s now an effective avenue for public opposition to be expressed. If a data center project is withdrawn or declined, most of the time it occurs during the rezoning process. If the property is already zoned to allow for the construction of the data center and the land is purchased for that purpose, historically, these projects could move forward under “by-right” development if they complied with all the codes and regulations. In the spring of 2025 many localities across the U.S., including Loudoun County, VA, however, have eliminated “by-right” development for data centers. Even if the data center has purchased the land and does not require a change in zoning or other special provisions, the projects must be considered and approved individually by the local authorities through a process including public hearings before construction.

- Public Interest: While there have always been residents who oppose development in their community, or oppose data centers specifically, the resistance to data centers has not only grown in number, but it has also become more sophisticated and organized. Environmental organizations and anti-data center development social media groups publish talking points and update residents on the latest news from local counties; these posts reach millions more people than any government website, flyer, or newspaper advertisement ever could. Their key concerns tend to be environmental impacts such as air pollution or water use, power needs and an anticipated increase in utility bills because of it, the confidential nature of several data center transactions, and quality of life concerns including noise, light pollution, traffic during construction, proximity to homes or schools, building aesthetics, tree and wildlife impacts, and general loss of rural nature.

- Water: The recent water regulatory landscape has been more dynamic related to data centers. For example, some localities are limiting water use by data centers or restricting construction projects that propose to draw a large quantity of water. At the state level, Ohio Environmental Protection Agency (OEPA) is looking at discharges, proposing a new type of NPDES general permit for both wastewater and stormwater discharges from data centers. The “NPDES General Permit for Discharges from Data Center Facilities” would cover data center facility operations that discharge to waters of the state. The draft permit is undergoing public review, but comments are expected to include pushback. More states may draft similar data center-specific NPDES permits if OEPA’s is approved.

Conclusion

Data centers carry the responsibility of housing data for the modern economy and the advancement of AI while also not only complying with existing requirements but keeping an eye on what the future brings. ALL4 is proud to partner with data centers all over the U.S. to support: site decisions, budget and equipment planning through air permit strategies, construction schedules through comprehensive and turnkey permitting efforts, noise monitoring and modeling, sustainability goals and reporting, health and safety needs, and compliance with environmental requirements through diligent reporting, training, tool development (including digital solutions), auditing, and more.

Need an air permit strategy mapping the interplay of turbines, fuel cells, and generators?

Need support with environmental talking points ahead of a public hearing?

Need noise modeling?

Check out our weekly newsletter and our Data Center page for more content from ALL4 this year.

Please reach out: Sharon Sadler, WDC Office Leader and ALL4 Data Center Sector Lead, at ssadler@all4inc.com or 571-392-2595.

US Power Sector: 2026 Lookahead

Author: Rich Hamel

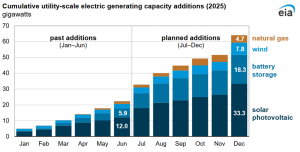

2025 was an interesting year in power in the United States, with the power sector expanding at breakneck speed driven by the rapid expansion of data centers and the energy needs to support artificial intelligence (AI). While the final numbers on capacity additions have not yet been published, if the projected numbers for the second half of 2025 were met, about 64 gigawatts (GW) of new electricity generating capacity will have been deployed, with more than half (33.3 GW) coming in the form of new solar photovoltaic generation, and over 18 GW of new battery storage:

Data source: U.S. Energy Information Administration, Preliminary Monthly Electric Generator Inventory, June 2025

Interestingly, according to the U.S. Solar Market Insight Q4 2025 report, 73% of all solar capacity installed was built in “red” states: Texas, Indiana, Florida, Arizona, Ohio, Utah, Kentucky, and Arkansas. 11.7 GW of solar power were installed in the 3rd quarter of 2025 alone.

Meanwhile, gas-fired power is being permitted as fast as the supply chain will allow, with about 5 GW of new capacity projected to have come online in 2025 and many new gas-fired power plants in various stages of the permitting process.

Battery power is also becoming a significant factor in the power industry, and at one point in March of 2025, 10% of the power on the Electric Reliability Council of Texas (ERCOT) grid was from battery storage, the first time this had ever happened.

In coal, the Trump administration issued Executive Order (EO) 14241 which was designed to reinvigorate the coal industry. While no new coal-fired generation was deployed or announced, just under 1 GW of coal-fired power that was scheduled to be retired has been extended through a number of Department of Energy 202(c) emergency orders requiring various coal-fired assets to stay online.

Where are we going?

According to ICF, electricity demand in the U.S. is expected to grow 25% by 2030 and 78% by 2050 compared to 2023 levels. In order to meet the 2030 total, the U.S. would need to deploy power at about twice the rate it currently is. Data centers alone are expected to require as much as 44 GW of new capacity.

According to Deloitte, to achieve these goals, investments of ~$1.4 trillion may be necessary. To get there, however, we are likely to need to see significant amounts of private equity investment, as the traditional route of raising capital for these projects, rate-based changes, is mostly maxed out and is not expected to cover this cost.

In terms of the capacity itself, where will it come from? At present, it appears that new gas-fired power is being deployed about as fast as it can, hindered primarily not by regulatory concerns but by supply chain as turbine vendors are currently back-ordered by several years. The Trump administration is actively putting the brakes on new renewable solar- and onshore and offshore wind-energy projects, having canceled over 226 GW of previously approved projects in 2025 alone. Coal doesn’t seem to be the answer with no new coal coming online or planned and less than 1 GW of previously scheduled-to-retire coal-fired units staying online. Nuclear, both in the form of large utility scale reactors and new small modular reactor (SMR) technology is coming, backed by billions of dollars of investment by hyper-scalers who need the power for their new data centers, but it’s still seemingly years away. How policy and the critical need for new generation intersect will be a key thing to watch in 2026.

Regulatory Direction

The Trump administration has signaled a deregulatory approach and in March of 2025 U.S. Environmental Protection Agency (U.S. EPA) Administrator Lee Zeldin announced the largest deregulatory action in U.S. history. For more on what has been referred to as the “31 flavors” and how those actions might impact the power sector, see our 4 The Record article. Most of these actions have taken form largely not in eliminating existing regulations, but in canceling or significantly reducing regulations that were proposed or in planning during the Biden Administration. The two most important of these to the power sector are:

- Revisions to Standards of Performance for New Stationary Sources (NSPS) for Stationary Combustion Turbines(revised Subparts GG and KKKK and new Subpart KKKKa at 40 CFR Part 60) were just finalized on January 15th and are now effective. As expected, the final Subpart KKKKa is less stringent than the proposed rule, with primary revisions being that the Best System of Emissions Reduction (BSER) is selective catalytic reduction (SCR) only for new, large, highly-utilized combustion turbines, and a new subcategory for temporary turbines that are in place for less than 24 months having a nitrogen oxides (NOX) limit of 25 parts per million (ppm) at 15% dioxygen (O2) or 0.092 pounds per million British Thermal Units (lb/MMBtu). There are two repercussions for the power industry, both positive: First, the determination that SCR is BSER only applies to highly utilized utility scale turbines, for which Best Available Control Technology (BACT) would almost always require SCR for NOX control regardless. Second, the split out of temporary turbines with a two-year time period at an emission rate that is easily achievable for most turbine types, such as 25 ppm, allows for a lot of flexibility for those projects that require temporary power while their permanent power source is being purchased and installed, especially data center projects. For a full discussion of what is in the revised rule, see our recent article on the topic.

- Standards of Performance for Greenhouse Gas (GHG) Emissions from Modified Coal-Fired Steam Electric Generating Units (EGUs) and New and Reconstructed Stationary Combustion Turbine EGUs (40 CFR Part 60, Subpart TTTTa) were promulgated in May 2024 but subsequently proposed for repeal or significant revision in June 2025. If the rule were to remain in place, it could significantly hamper gas-fired power generation as many new turbines would need to be limited to low-capacity factors in order to comply with the GHG limits. U.S. EPA was originally expected to promulgate a final rule in December 2025 but the government shutdown caused a delay and we now expect to see a final rule sometime in the first half of 2026, following a decision on the fate of the GHG endangerment finding. While the lack of a decision on Subpart TTTTa has caused a delay in submittal of permit applications or issuance of permits for some projects given the associated uncertainty about an achievable BACT standard that accommodates high utilization and the possibility of low load operation, the expectation is that Subpart TTTTa, along with a number of other GHG standards, will be repealed or significantly revised eventually.

For more insight on expected changes to other environmental regulations, see our air and water lookahead articles.

Power Sector in 2026

Regardless of any regulatory changes, ALL4 continues to see several fast-track programs bring new gas-fired power generating facilities online, including the PJM regional transmission organization (RTO)’s Reliability Resource Initiative, and Midcontinent Independent System Operator’s (MISO) similar proposed Expedited Resource Adequacy Study (ERAS) program for its region. These fast-track programs are tempered by the fact that large turbine vendors in the U.S. are currently backlogged on combustion turbine orders for two or more years, with no relief in sight. The supply chain concerns are further exacerbated by cost concerns associated with general confusion about the administration’s tariff program and associated international trade issues. Additionally, despite the critical need for additional electricity generation, many power projects, especially gas-fired power, continue to face significant public opposition, which not only adds more challenges to completing the permitting process but may also cause lengthy delays as permits get appealed.

Regardless of these challenges, utilities, power developers, and data center developers are expected to continue to permit and construct facilities as fast as the permitting process and supply chain for equipment will let them. We also expect to see companies investing more in the deployment of large-scale Reciprocating Internal Combustion Engines (RICE) for electricity generation, as well as increased deployment of fuel-cell technology as industry explores ways to get power to the grid as quickly as possible.

ALL4 will continue to track developments in regulatory and technical requirements related to the power sector in an era of expanding demand growth. ALL4 has significant power sector experience related to the entire life cycle of a power project, from due diligence and site selection to permitting and modeling, then to commissioning and ongoing compliance for electricity-generating facilities of all fuel types. That experience is combined with our established working relationships with numerous state agencies and U.S. EPA. ALL4 provides a full range of environmental, health and safety (EHS), and data services to our clients to help them meet their permitting, monitoring, testing, recordkeeping, and reporting challenges. If you’d like to learn more about our capabilities in the power sector, please contact Rich Hamel or your ALL4 project manager and stay tuned for the debut of our quarterly power sector newsletter, coming soon!

2026 Chemical Sector Lookahead

Author: Philip Crawford

At the end of 2024 there were numerous regulatory developments impacting the chemical manufacturing industry. For many, it felt like a nonstop stream of changes that were going to significantly impact the legacy compliance programs of their facilities. In 2025, with the change in administration, the U.S. Environmental Protection Agency (U.S. EPA) shifted to a deregulatory focus. However, with the full agenda and the government shutdown, not many of the stated deregulatory priorities were achieved in 2025. Now that we are entering 2026, we are expecting to see progress in the form of proposed and final rules that will scale back or remove completely the changes that were completed during the previous administration. Additionally, there remain some consent decree driven deadlines that U.S. EPA must meet that will have impacts on the industry. This lookahead article briefly touches on several of the more significant actions we expect the agency to take in 2026.

PEPO, CMAS, HON

What’s on the horizon for chemical sector air regulations in 2026? As of the writing of this article the course ahead is still a little foggy, but we expect that fog to somewhat recede early this year whenU.S. EPA finalizes changes to the National Emission Standards for Hazardous Air Pollutants (NESHAP) for Chemical Manufacturing Area Sources (CMAS) on February 27, 2026. Shortly after, U.S. EPA is expected to finalize changes resulting from a risk and technology review (RTR) for the NESHAP for Polyether Polyols Production (PEPO) on March 13, 2026.

U.S. EPA initially proposed significant changes to the PEPO rule on December 27, 2024 to address perceived risk from ethylene oxide (EtO), incorporate updates in technology, and address regulatory gaps. On January 22, 2025, U.S. EPA proposed changes to the CMAS rule. Like the PEPO proposal, U.S. EPA proposed changes to regulate emissions of EtO, address developments in technology, revise testing and reporting requirements, and remove affirmative defense provisions. Both of these proposals followed in the wake of U.S. EPA’s sweeping changes to the NESHAP for Synthetic Organic Chemical Manufacturing Industry (SOCMI) and Group I and II Polymers and Resins (P&R I and II) Industries (known as The HON and P&R I and II) that were finalized on May 16, 2024. U.S. EPA heavily referenced the new and revised provisions in the HON rule to incorporate these proposed changes into the PEPO proposal, and to a lesser extent, the CMAS proposal.

As we previously summarized in the PEPO/CMAS article linked above, both the PEPO and CMAS proposals contained new emissions standards for EtO from sources such as process vents, equipment leaks, storage tanks, heat exchange systems, and wastewater. Both proposals also contained fenceline monitoring provisions for EtO by reference to the HON rule. Individual companies and industry associations submitted numerous comments on the proposed EtO control standards during each respective comment period. Commenters also provided U.S. EPA with input on several non-EtO related portions of the proposed rule. Although we expect to see several differences from proposal to final, we won’t speculate on them here. Expect to see another article in about a month or so with details on the final CMAS rule and insights on the upcoming final PEPO rule.

We also expect U.S. EPA to issue a proposed reconsideration rule for several aspects of the 2024 HON updates sometime in mid-2026. Multiple industry associations and individual companies submitted petitions requesting U.S. EPA reconsider the use of the EtO Integrated Risk Information System (IRIS) value, the risk assessment methodology, the fenceline monitoring requirements, EtO control requirements, startup and shutdown provisions, the removal of the total resource effectiveness concept, and several other provisions. Because of the overlap between the HON and PEPO rules, we expect that the upcoming PEPO final rule will provide a reasonable prediction of the changes to expect in the HON reconsideration proposal. The reconsideration proposal included additional requests for the SOCMI New Source Performance Standards (NSPS, Subparts IIIa, NNNa, RRRa) and P&R II, but it remains unclear how U.S. EPA plans to address those requests or if we will see a reconsideration proposal in 2026.

As a reminder, facilities subject to the EtO provisions of the final HON rule must be in compliance with those requirements no later than July 15, 2026. Additionally, facilities subject to the fenceline monitoring requirements in the HON must start collecting data by July 15, 2026, although the requirements to implement corrective actions do not apply until July 2027. Keep in mind that even though we may see a proposed HON reconsideration rule from U.S. EPA by July of this year, a final rule is still another several months away after the proposal.

NSPS Kc

We also expect to see a proposed reconsideration rule for the Standards of Performance for Volatile Organic Liquid Storage Vessels (Including Petroleum Liquid Storage Vessels) for Which Construction, Reconstruction, or Modification Commenced After October 4, 2023 (40 CFR Part 60, Subpart Kc). The original rule was published on October 15, 2024 and contained several changes compared to Subpart Kb, the legacy New Source Performance Standard (NSPS) applicable to volatile organic liquid storage tanks. We detailed those changes in a previous article, but most notable was U.S. EPA’s revised interpretation of a modification as it applies to storage vessels, new air emissions control requirements, degassing requirements for certain tanks, and a variety of new inspection, monitoring, performance testing, and recordkeeping requirements.

A petition for reconsideration was submitted by industry in December 2024 and U.S. EPA granted reconsideration in April 2025. The petition covered items such as the definition of modification, control requirements for both internal and external floating roof tanks, and clarifications around degassing requirements, to name a few. We expect U.S. EPA to issue a proposed reconsideration rule addressing the petitioners’ concerns in the spring of this year, but those facilities with tanks subject to Subpart Kc must continue to comply with the provisions as they currently stand until U.S. EPA finalizes the reconsideration rule, which we expect to occur sometime in 2027. If you have questions on applicability or how to comply with Subpart Kc in the meantime, check out the “frequently asked questions” page published by U.S. EPA in April 2025, or reach out to your ALL4 project manager or Philip Crawford at pcrawford@all4inc.com.

HWC MACT

U.S. EPA proposed revisions to 40 CFR Part 63, Subpart EEE: NESHAP from Hazardous Waste Combustors (HWC MACT) on November 11, 2025. We discussed U.S. EPA’s proposed changes in an article published earlier this month. The changes included an emissions limit for hydrogen fluoride (HF) for solid fuel boilers and work practices to limit HF from liquid fuel boilers. U.S. EPA also proposed hydrogen cyanide (HCN) limits for solid and liquid fuel boilers, as well as cement kilns. The proposed revisions also include replacement of the startup, shutdown, and malfunction (SSM) exemption with work practice standards for periods of SSM; electronic reporting requirements; and an allowance for states to exclude HWC that are considered area sources from the requirement to obtain a Title V permit if the facility’s Resource and Conservation Recovery Act (RCRA) permit is revised accordingly. While the impacts of the proposed changes are expected to be minimal, entities who are operating HWC MACT applicable sources should spend time understanding the potential implications of the proposed changes and watch the final rule closely to verify they will be able to comply with the final requirements. We expect to see the final rule published sometime in 2026.

Other Updates

The Risk Management Program (RMP) rule was originally issued in 1996. Substantial changes were proposed and finalized in 2017 but were rolled back in 2019. Changes were once again proposed in 2022 and finalized in March 2024. The proposed updated RMP rule was recently reviewed by the White House Office of Management and Budget (OMB) so we will see it any day now. We expect that the revised rule will be closer to the 2019 version of the RMP rule than the 2024 version, given the current administration’s lack of focus on the environmental justice and climate change issues that prompted many of the recent revisions.

The 2024 changes to the rule that reversed the once in, always in policy, or “Reclassification of Major Sources as Area Sources Under Section 112 of the Clean Air Act” (MM2A) Rule, were eliminated in 2025 through a Congressional Review Act (CRA) resolution and a recent Federal Register notice officially reverted the rule to its 2020 form. Original litigation on the 2020 MM2A rule had been halted upon completion of the September 2024 final rule. With the CRA signed and that rule no longer in effect, litigation on the 2020 MM2A rule is now moving ahead. It’s not clear what the results of that litigation will be, but we are continuing to monitor this regulation. Currently, under the 2020 MM2A rule, major sources of hazardous air pollutants (HAP) can reclassify to area source status if their emissions are below the HAP major source thresholds.

In December 2024, U.S. EPA finalized risk management rules for three chemicals under the Toxic Substances Control Act (TSCA): Carbon Tetrachloride (CTC), Perchloroethylene (PCE), and Trichlorethylene (TCE). U.S. EPA has since indicated they are reconsidering at least some aspects of each of these rules – accepting public comment for CTC and PCE reconsideration and TCE extending compliance dates for two use cases. In the case of both CTC and PCE, U.S. EPA has already said that this is just the first step in their efforts to reconsider, and possibly revise, the risk management rules. The impacts of a typical Risk Management Rule are near total ban of chemical manufacture or import, phase down of “essential” uses, and implementation of Workplace Chemical Protection Program (WCPP). We will be watching the reconsideration of these recent TSCA risk management rules to see what changes U.S. EPA proposes.

If you’d like to learn more about TSCA updates, see the our article U.S. EPA Seeks Public Comment on Updated Draft Formaldehyde Risk Calculation Memorandum to Inform Risk Evaluation under the Toxic Substance Control Act. In addition to the items discussed in this article, ALL4’s lookahead article series includes information on other relevant topics, such as the Clean Water Act Hazardous Substances Facility Response Plan Rule, Resource Conservation and Recovery Act (RCRA) updates, and changes expected from the Occupational Safety and Health Administration (OSHA). ALL4 has staff in our Environmental, Health, and Safety (EHS) practice that can help you understand the implications of each of these areas.

Conclusion

With any of the changes on the horizon, there is likely to be litigation, so it will take time to see what regulatory updates are permanent. ALL4 has a large and experienced air quality consulting practice, and we continuously monitor federal and state air regulatory developments and participate in industry association advocacy efforts. Our EHS experts also monitor changes to the non-air regulations that impact the chemical industry. We can help you comment on regulatory proposals and draft policies, evaluate how regulatory changes could affect your facility, strategize on how to implement new regulations or permit projects, navigate permit changes to your facility, implement new regulations and permit requirements, and track ongoing compliance with requirements. Please reach out to your ALL4 project manager, Philip Crawford, or Julie Taccino with any questions or if you need EHS consulting support.

U.S. EPA Finalizes Combustion Turbine NSPS Revisions

Author: Caleb Fetner

Less than one week after being signed by U.S. Environmental Protection Agency (U.S. EPA) Administrator Lee Zeldin, the Combustion Turbine New Source Performance Standards (NSPS) revisions were published in the Federal Register on January 15, 2026 and thus, are now effective.

This final rulemaking establishes emissions standards and compliance schedules under 40 CFR Part 60, Subpart KKKKa for stationary combustion turbines that are constructed, modified, or reconstructed after December 13, 2024. The final rule publication also includes revisions to 40 CFR Part 60, Subparts GG and KKKK. Specifically, this rule:

- Establishes nitrogen oxides (NOX) emissions standards for various combustion turbine size, utilization, and design efficiency subcategories;

- Determines that selective catalytic reduction (SCR) is the best system of emissions reduction (BSER) for new, large combustion turbines with a high utilization rate (> 45 percent);

- Concludes that continued use of combustion controls is the BSER for limiting NOX emissions from all other combustion turbine subcategories;

- Retains the sulfur dioxide (SO2) standards from Subpart KKKK; and

- Does not establish standards for any new criteria pollutants, including particulate matter (PM/PM10 /PM5) or carbon monoxide (CO).

As rapid expansion in the power generation and data center sectors continues to fuel growth in the combustion turbine market, the much-anticipated final rule is, as expected, less stringent than the proposed rule issued at the end of the previous Administration. The rulemaking notice also states that the action is considered a deregulatory action under Executive Order 14192: Unleashing Prosperity Through Deregulation and is generally aligned with the current Administration’s “Unleashing American Energy” initiative.

NOX Emissions Standards

As originally proposed, U.S. EPA sought to not only change the size-based subcategories under Subpart KKKK but also further subcategorize sources by capacity utilization (i.e., low, intermediate, or high load), consistent with 40 CFR Part 60, Subpart TTTTa (which U.S. EPA has since proposed to repeal on June 1, 2025).

After considering comments that criticized both the size-based subcategory revisions and the addition of utilization-based subcategories, U.S EPA decided to:

- Retain the size-based subcategories from Subpart KKKK;

- Shift to just two utilization-based subcategories for large and medium turbines aimed at distinguishing between simple cycle and combined cycle turbines: high-utilization (> 45%) and low-utilization (≤ 45%); and

- Introduce new subcategories based on the manufacturer’s design efficiency for large, low-utilization combustion turbines.

The following table summarizes the Subpart KKKKa NOX emissions standards for the different subcategories established in the final rule.

| Combustion Turbine Size | Combustion Turbine Type | Utilization Rate(a) | Manufacturer Design Efficiency | BSER | Input-Based NOX Emission Standard (4-hour rolling average) |

Optional Output-Based NOX Emission Standard (30-operating-day average) |

||

| ppm at 15% O2 | lb/MMBtu | lb/MWh-gross | lb/MMh-net | |||||

| Large (> 850 MMBtu/h) | New, firing natural gas | High ( > 45%) | All | SCR | 5 | 0.018 | 0.12 | 0.12 |

| New, firing natural gas | Low (≤ 45%) | High (≥ 38%) | Combustion Controls | 25 | 0.092 | 0.83 | 0.85 | |

| New, firing natural gas | Low (≤ 45%) | Low (< 38%) | Combustion Controls | 9 | 0.033 | 0.37 | 0.38 | |

| Modified or reconstructed, firing natural gas | All | High (≥ 38%) | Combustion Controls | 25 | 0.092 | 0.83 | 0.85 | |

| Modified or reconstructed, firing natural gas | All | Low (< 38%) | Combustion Controls | 15 | 0.055 | 0.62 | (b) | |

| New, modified, or reconstructed, firing non-natural gas | All | All | Combustion Controls | 42 | 0.16 | 1.0 | 1.0 | |

| Medium (> 50 MMBtu/h and ≤ 850 MMBtu/h) | New, firing natural gas | High ( > 45%) | All | Combustion Controls | 15 | 0.055 | 0.43 | 0.44 |

| New, firing natural gas | Low (≤ 45%) | All | Combustion Controls | 25 | 0.092 | 1.2 | 1.2 | |

| New, firing non-natural gas | All | All | Combustion Controls | 74 | 0.29 | 3.6 | 3.7 | |

| Medium (> 20 MMBtu/h and ≤ 850 MMBtu/h) | Modified or reconstructed, firing natural gas | All | All | Combustion Controls | 42 | 0.15 | 2.0 | 2.0 |

| Modified or reconstructed, firing non-natural gas | All | All | Combustion Controls | 96 | 0.37 | 4.7 | 4.8 | |

| Small (≤ 50 MMBtu/h) | New, firing natural gas | All | All | Combustion Controls | 25 | 0.092 | 1.4 | 1.4 |

| New, firing non-natural gas | All | All | Combustion Controls | 96 | 0.37 | 5.3 | 5.4 | |

| Small (≤ 20 MMBtu/h) | Modified or reconstructed, all fuels | All | All | Combustion Controls | 150 | 0.55 | 8.7 | 8.9 |

| > 50 MMBtu/h | New, firing natural gas, either offshore turbines, turbines bypassing the heat recovery unit, and/or temporary turbines | All | All | Combustion Controls | 25 | 0.092 | N/A | |

| ≤ 300 MMBtu/h | Located north of the Arctic Circle (latitude 66.5 degrees north), operating at ambient temperatures less than 0°F (-18°C), modified or reconstructed offshore turbines, operated during periods of turbine tuning, byproduct-fired turbines, and/or operating at less than 70 percent of the base load rating | All | All | Combustion Controls | 150 | 0.55 | N/A | |

| > 300 MMBtu/h | Located north of the Arctic Circle (latitude 66.5 degrees north), operating at ambient temperatures less than 0°F (-18°C), modified or reconstructed offshore turbines, operated during periods of turbine tuning, byproduct-fired turbines, and/or operating at less than 70 percent of the base load rating | All | All | Combustion Controls | 96 | 0.35 | N/A | |

| All sizes | Heat recovery units operating independent of the combustion turbine | N/A | 54 | 0.20 | N/A | |||

(a)Utilization rate under Subpart KKKKa is determined based on 12-calendar-month annual capacity factor, defined as the ratio between the actual heat input to a stationary combustion turbine during a calendar year and the potential heat input to the stationary combustion turbine had it been operated for 8,760 hours during a calendar year at the base load rating.

(b) 0.30 lb/MW-net is listed in the final regulatory text in the docket, but is an apparent typo in the conversion of 0.29 kg/MWh-net to pounds.

Large Combustion Turbines

Large combustion turbines are defined as having a base load rated heat input greater than 850 million British thermal units per hour (MMBtu/h) on a higher heating value (HHV) basis. In a change from the proposed rule, U.S. EPA decided that there was no difference in combustion control reasonableness between “low” and “intermediate” load turbines and decided to change the three proposed utilization subcategories into just two. Generally, large, natural gas-fired, combustion turbines are now subcategorized as high-utilization or low-utilization based on whether the 12-calendar-month capacity factor exceeds 45 percent. Although not specifically defined as simple cycle versus combined cycle, the 45 percent cutoff was roughly based on the 99 percent confidence, maximum 12-calendar-month capacity factor for recently constructed simple cycle turbines. U.S. EPA also included provisions in Subpart KKKKa to exclude operation during system emergencies (i.e., Reliability Coordinator has declared an Energy Emergency Alert level 1, 2, or 3) from the utilization subcategorization.

U.S. EPA has reversed its proposal that SCR is cost-effective for combustion turbines larger than 250 MMBtu/h and now has determined that combustion controls is BSER for most turbine subcategories. SCR is now only considered BSER for large, high-utilization combustion turbines. U.S. EPA also relaxed the proposed standard of 3 parts per million (ppm) for these turbines to 5 ppm, noting that the 5 ppm emissions standard will allow facilities to use higher efficiency (and therefore higher NOX-emitting) turbines that will result in less environmental impact due to less fuel use and less ammonia slip. Although some combustion turbines are capable of meeting 2 to 3 ppm [new sources may still be subject to a more stringent Best Achievable Control Technology (BACT) limit], U.S. EPA determined that that the 5 ppm standard is achievable for all turbines in this subcategory.

In another change from the proposed rule, U.S. EPA has further subcategorized large, low-utilization turbines as high-efficiency and low-efficiency, based on a manufacturer-provided design efficiency cutoff of 38 percent, on a high heating value (HHV) basis. This subcategorization accounts for the tradeoff that exists for turbine manufacturers: design choices that improve efficiency also create conditions that favor NOX formation (e.g., higher temperatures and pressures).

Medium Combustion Turbines

A medium combustion turbine is defined under Subpart KKKKa as a stationary combustion turbine with a base load rating greater than 50 MMBtu/h and less than or equal to 850 MMBtu/h of heat input. However, the rule also establishes a lower cutoff of 20 MMBtu/hr for modified or reconstruction sources because combustion controls that achieve the 25 ppm NOX standard may not be available for all existing small combustion turbines that are modified or reconstructed. U.S. EPA did not further subcategorize based on design efficiency as there generally aren’t high efficiency (> 38 percent) turbines of this size.

Small Combustion Turbines

U.S. EPA removed any utilization-based subcategories for small combustion turbines and set the natural gas-fired standard for new sources at 25 ppm, based on the common manufacturer-guaranteed value for turbines in this size category using dry combustion controls.

Partial Load Standards and Alternative Mass-Based Standards

As provided in Table 1, Subpart KKKKa establishes less stringent NOX standards for turbines that are operating at 70 percent or less of their base load rating. The applicable NOX standard is determined on an operating-hour basis, and if the turbine is operated at partial load at any point during the hour, then the partial load standard applies for the entire hour.

Short-term (4-hour) and long-term (12-month) mass-based NOX standards (mass NOX per MW-rated output) are added as optional alternatives to the input- and output-based NOX standards. The mass-based standards are favorable in scenarios where high-efficiency, simple cycle turbines with SCR want to operate in excess of the 45 percent utilization rate and maintain compliance with the applicable standards.

Proposed Reconstruction Definition Not Finalized

In the December 2024 version, U.S. EPA proposed that only the combustion turbine portion of the affected source would be considered when evaluating whether the affected source is reconstructed. The comprehensive definition of “stationary combustion turbine” under 40 CFR §60.4420 (and now 40 CFR §60.4420a) includes the heat recovery steam generator (HRSG) and associated duct burners at combined cycle and combined heat and power CHP facilities. Those definitions are used when determining if an affected facility is reconstructed. Under U.S. EPA’s originally proposed approach, if the fixed capital cost of just the new combustion turbine engine components for a combined cycle turbine exceeded 50% of the cost of just a new combustion turbine engine, then the entire affected source (i.e., the entire combined cycle system) would have met the proposed reconstruction criteria and would have been subject to Subpart KKKKa. This was also, notably, in conjunction with U.S. EPA proposing to set the NOX emissions standards for reconstructed sources equal to the standards for new sources, believing that reconstructed turbines could likely incorporate the same NOX reduction technologies at similar costs compared to a greenfield facility.

ALL4 assisted several clients and industry associations in developing comments on the originally proposed more-restrictive reconstruction definition and emissions standards, which primarily took issue with the proposal’s intent to classify refurbishments to a portion of the affected source as substantially equivalent to constructing an entirely new affected source. With renewed emphasis on the underlying statutory language behind Federal agencies’ interpretations stemming from Loper Bright Enterprises v. Raimondo, 144 S. Ct. 2244 (2024), some industry commenters also pointed out that Section 111 of the Clean Air Act (CAA) only authorizes U.S. EPA to establish NSPS for newly constructed and modified sources (in contrast with CAA Section 112 which includes reconstruction in the definition of a new source]). Commenters also argued that the NOX standards for reconstructed units should be equal to the standards for modified sources because the same retrofit technology limitations and costs for modifications apply to reconstruction.

Ultimately, U.S. EPA excluded the proposed reconstruction definition from the final Subpart KKKKa rulemaking. U.S. EPA also agreed with commenters that “the costs of retrofitting combustion turbines with SCR is significantly higher than for new sources” and aligned the standards for modified and reconstructed sources as provided in Table 1.

New Subcategory for Temporary Turbines

After soliciting comments on creating either a subcategory or an exemption for temporary turbines, U.S. EPA has finalized a new subcategory in Subpart KKKKa for small and medium stationary temporary combustion turbines that meet the following criteria:

- The turbine must have a base load rating less than or equal to 850 MMBtu/hr (i.e., a small or medium turbine).

- The turbine may only be located at the same stationary source (or group of stationary sources located within a contiguous area and under common control) for a total period of 24 consecutive months. The clock starts after the turbine commences operation at a location and continues regardless of whether the turbine operates for the entire 24-month period.

- Any temporary combustion turbine that replaces a temporary combustion turbine at a location and performs the same or similar function will be included in calculating the consecutive time period.

- The relocation of a stationary temporary combustion turbine within a single stationary source (or group of stationary sources located within a contiguous area and under common control) while performing the same or similar function (e., serving the same electric, mechanical, or thermal load) does not restart the 24-calendar month residence time period.

Stationary temporary combustion turbines must comply with the following requirements:

- Each temporary turbine must have a manufacturer’s emissions guarantee to meet a NOX emissions standard of 25 ppm at 15% O2 or 0.092 lb/MMBtu.

- Each temporary turbine must have been performance tested at least once in the prior 5 years meeting this NOX emissions standard.

- The otherwise applicable SO2 standard and fuel sulfur content recordkeeping will apply.

U.S. EPA initially considered a 12-month period for the temporary turbine subcategory but finalized with the 24-month period, agreeing with commenters recommendations to account for situations requiring temporary power generation lasting longer than 12-months. U.S. EPA also noted that a 24-month period is consistent with Prevention of Significant Deterioration (PSD) policy that recognizes that emissions occuring for less than 24-months are temporary and excluded from some aspects of PSD review since their ambient air impacts are short-lived.

In the preamble to the final rule, U.S. EPA explained that the creation of the temporary turbine subcategory facilitates reducing the permitting burden for these types of turbines, for both minor NSR permitting – through States potentially establishing a general permit or a permit by rule (PBR) for temporary turbines – as well as major NSR permitting, by assisting States in clearly identifying temporary emissions that may be excluded from certain air quality modeling demonstrations under 40 CFR 52.21(i)(3)(ii).

Based on ALL4’s review of the regulatory language posted to the docket, U.S EPA’s introduction of the temporary generator subcategory, although well-intended, may have created some confusion due to inconsistencies between the preamble and the regulatory language. In the preamble, U.S. EPA states that a 74 ppm NOX emissions standard would apply to temporary turbines burning non-natural gas fuels, but the regulatory text for Subpart KKKKa provided in the docket does not appear to establish a non-natural gas NOX standard for temporary turbines. Similarly, U.S. EPA added the temporary combustion turbine requirements under Subpart KKKK but did not explicitly add the temporary combustion turbine NOX emissions standard to Table 1 to Subpart KKKK. ALL4 will be monitoring the docket closely as more files are added for any administrative updates addressing these inconsistencies, as well as the apparent typo in Table 1 to Subpart KKKKa footnoted in the table above.

Finally, U.S. EPA included language in Subparts GG, KKKK, and KKKKa that excludes portable combustion turbines from the definition of the affected source if portable combustion turbines were to be regulated as a “nonroad engine” under Title II of the CAA.

Conclusion

As U.S. is expecting a drastic step-change in electricity demand over the next five years and natural gas-fired generation is being developed as quickly as the supply chain allows, Subpart KKKKa will be impactful to multiple industries evaluating new stationary combustion turbines, including utilities and data centers. ALL4 is continuing to help our clients evaluate compliance strategies for Subpart KKKKa and the entire lifecycle of greenfield generation projects, including siting, permitting, commissioning, and ongoing compliance. Please reach out to me or ALL4’s Power Sector Lead Rich Hamel to learn more.

2026 Climate Reporting Look Ahead: Navigating the Regulatory Divergence

Author: Louise Shaffer

2026 might be a year that has the most complex compliance crossroads in the history of environmental regulation, especially in regard to climate regulations. As ALL4 predicted in 2025, the regulatory environment has fractured into two distinct, competing trajectories for climate reporting. On one hand, we are seeing the Federal government’s desire to deregulate greenhouse gas (GHG) emissions and withdraw from climate organizations; on the other, states like California and New York have moved to the enforcement phase of their own 2025 proposed climate-related regulations. International regulations such as the European Union (EU) Corporate Sustainability Reporting Directive (CSRD) continue to change and significantly simplify sustainability reporting requirements in the EU. The incongruity across all these regulatory bodies makes 2026 a difficult landscape to navigate for companies, potentially adding to the reporting burden.

Climate regulations encompass a wide range of categories from GHG emissions reporting, climate risk reporting, and circular economy regulations. This Look Ahead will outline some of the items that your company should watch out for in 2026.

1. Federal Rollbacks

The Federal deregulation of GHG emissions is rooted in the proposed rescission of the 2009 Endangerment Finding. The 2009 Endangerment Finding is the legal basis for GHG emissions being regulated under the Clean Air Act because it determined that GHG emissions are a threat to public health and welfare. If the United States Environmental Protection Agency (U.S. EPA) successfully revokes the 2009 Endangerment Finding in 2026, the legal floor falls out from under almost every Federal climate regulation. It would mean that GHGs do not meet the Clean Air Act’s definition of air pollutant, effectively blocking U.S. EPA’s authority to demand GHG data or set emissions standards. The repeal of the 2009 Endangerment Finding is currently at the Office of Management and Budget for review. At this time, U.S. EPA has two other proposed GHG rule reconsiderations that include the Federal GHG Reporting Program under 40 CFR Part 98 and the GHG Standards for Fossil Fuel-Fired Power Plants under the 40 CFR Part 60 Standards of Performance for New Stationary Sources (NSPS) and Emission Guidelines.

On September 16, 2025, U.S. EPA published a proposed rule to reconsider the GHG Reporting Program (GHGRP) under 40 CFR Part 98. This rule currently requires certain facilities that emit over 25,000 metric tons of carbon dioxide equivalent (MT CO2e) annually to report their direct GHG emissions on an annual basis. While the 8,000 facilities that report under the GHGRP represent over 50% of U.S. emissions, this proposed deregulatory action risks obscuring national data trends and triggering a wave of non-uniform state mandates. Some of these states refer to 40 CFR Part 98 requirements but are sometimes more stringent. Consequently, multi-state organizations must prepare for a more fragmented compliance environment characterized by redundant recordkeeping and varying jurisdictional requirements based on each state in which they operate. It will be important for companies to continue to track their GHG emissions to prepare for emerging state regulations; this will be outlined in more detail in the next section.

On June 11, 2025, U.S. EPA proposed to repeal or significantly revise all GHG emissions standards for fossil fuel-fired power plants. This will affect facilities that are currently or have planned projects subject to 40 CFR Part 60, Subparts TTTT, TTTTa, or UUUUb. The proposed repeal or revision of the GHG standards creates a high level of uncertainty for power plants in particular, especially with the growing demand for electricity and new generation due to the surging baseload requirements coming from Artificial Intelligence (AI) and datacenter industries.

2. Emerging State REporting

While Federal GHG requirements face potential rescission, New York and California have stepped in as the nation’s climate regulatory leaders at the state level. In 2025, California passed two climate transparency regulations that continue to move forward despite legal hurdles. Senate Bill (SB) 253 (The Climate Corporate Data Accountability Act) remains in full effect, requiring companies with over $1 billion in annual revenue to disclose their Scope 1 and Scope 2 emissions by August 10, 2026, while Scope 3 reporting is not mandated until 2027. It is important for companies to start gathering this data at the beginning of 2026 to ensure ample time to collect all the necessary information.

Simultaneously, SB 261 (The Climate-Related Financial Risk Act), which targets companies with over $500 million in revenue, is navigating a complex legal landscape. The first reports for SB 261 were due January 1, 2026, but on November 18, 2025, the Ninth Circuit Court of Appeals granted a preliminary injunction that temporarily halted the enforcement of this rule. Legal arguments took place on January 9, 2026, and ALL4 will continue to follow the litigation of this rule throughout 2026. Currently, about 50 companies have voluntarily reported their climate risk assessments while the ongoing litigation occurs. While many companies are continuing to report voluntarily to maintain investor confidence, ALL4 advises all applicable entities to keep their climate risk assessments shelf-ready. A favorable ruling for the State could result in a reinstated deadline with a very short compliance window. Regardless of the regulatory drivers, having a climate risk assessment can help with business resilience over the coming years.

In 2025, New York State proposed similar Senate Bills to California SB 253 and SB 261, but these did not end up passing through the New York legislature last year. It is possible that similar Senate Bills will be brought to the New York State legislature again in 2026, especially if the California Climate Disclosure rules become final. In late 2025, the New York State Department of Environmental Conversation (NYSDEC) finalized 6 NYCRR Part 253 (Mandatory GHG Reporting Rule). While this rule mirrors the Federal GHGRP’s focus on facility-level, direct emissions (only Scope 1), California’s Climate Disclosures requires corporate inventories that encompass both direct (Scope 1) and indirect (Scope 2 and 3) emissions reporting. The New York Mandatory GHG Reporting Rule introduces heightened stringency for specific sectors. Most notably, the reporting threshold is 10,000 MTCO2e annually, which is lower than the Federal 25,000 MTCO2e threshold, capturing a significantly larger pool of mid-tier emitters previously exempt from Federal reporting. 2026 will be the first reporting year for the NY Mandatory GHG Reporting Rule, so we recommend facilities start collecting the extensive records required by the rule and determine your applicability. To ensure compliance, it is important for facilities to confirm applicability early in the year and finalize a comprehensive GHG Monitoring Plan (GHGMP) for submission by the December 31, 2026 deadline.

The emergence of these independent state frameworks signals a shift in the United States environmental regulatory climate, but it also creates a significant compliance issue for multi-state operators. While New York and California currently lead the charge with finalized rules, they are the first of many states to do so and have inspired others. ALL4 is closely monitoring the progression of Illinois HB 3673 (Climate Corporate Accountability Act) and New Jersey SB 4117 (Climate Corporate Data Accountability Act), both of which seek to impose their own $1 billion revenue thresholds and mandatory Scope 1, 2, and 3 disclosures.

3. International Reporting

There are also changes to climate regulations occurring internationally in 2025 which will affect 2026 reporting. These regulations will affect global companies and companies that export to the EU. The EU’s CSRD remains a dominant force for companies with European operations and 2026 will allow for less regulatory burden for U.S.-based parent companies in regard to the CSRD. Recent legislative shifts, including the Stop-the-Clock Directive and the 2025 Omnibus simplification package, have effectively delayed consolidated global reporting for most non-EU corporations until 2029. This delay reflects a broader EU effort to balance sustainability goals with economic competitiveness.

However, this simplification is offset by the entry of the Carbon Border Adjustment Mechanism (CBAM) into its final phase on January 1, 2026. For U.S. exporters in carbon-intensive sectors, specifically steel, aluminum, cement, fertilizers, and hydrogen, 2026 marks the end of the reporting only transition period. Starting this year, importers of these goods into the EU must now be registered as “Authorized CBAM Declarants” and will begin to have financial liabilities associated with the embedded carbon of their products. As the EU begins to phase out free emissions allowances for its own domestic producers, the cost of CBAM certificates will become a permanent factor in international trade.

The primary strategic challenge for 2026 is managing the tension between these EU requirements and the evolving U.S. requirements. As companies navigate a fragmented landscape of California disclosure mandates, New York facility-level rules, and Europe’s carbon-tax, the risk of non-uniform disclosures has never been higher. For forward-looking organizations, 2026 is less about meeting a single standard and more about building a unified data structure that can satisfy a patchwork of international/national requirements and carbon taxes without redundant administrative costs.

4. Circular Economy ─ Extended Producer Responsibility

Extended Producer Responsibility (EPR) laws are gaining traction throughout the United States. These laws vary in what products they apply to ─ ranging from batteries to single-use products. The regulations that are impacting the circular economy most are consumer packaging regulations. These EPR regulations cover a wide range of industries and will need ample stakeholder engagement as they emerge in more states. The goal of the regulations is to have the producer pay for the end use of the packaging, which will then help fund recycling programs and municipal waste handling infrastructure to manage the waste packaging. Currently in the U.S., the central EPR system is the Producer Responsibility Organization (PRO), which is a nonprofit entity that manages compliance, data reporting, and fee collection on behalf of all member producers. In most states, the Circular Action Alliance (CAA) has been appointed as the single approved PRO to harmonize these requirements across different jurisdictions. The goal is to have one organization unify the regulations, but there are already some differences in Oregon, Colorado, and California reporting requirements.

If your company sells consumer products in any of the following states, it will be important to start contacting stakeholders and gathering the necessary information to stay in compliance with these new regulations:

- Oregon: The first program to go live (July 2025), with 2026 marking the first full year of operational fee payments.

- Colorado: Program officially launched on January 1, 2026, with producer dues now being remitted to the CAA.

- California: While reporting began in late 2025, 2026 is a critical year for rulemaking and verifying your data ahead of the 2027 reporting and fee requirements.

- Maine and Minnesota: Programs still in the proposed rule phase, with 2026 deadlines for PRO registration and the initial reporting of packaging volumes occurring in 2027.

- Maryland and Washington: Both states have enacted laws and are currently conducting “Needs Assessments” to define the specific fee structures that will take effect in coming years.

- Connecticut, Hawaii, Illinois, Massachusetts, Michigan, Nebraska, New Jersey, New York, North Carolina, Rhode Island, and Tennessee: Introduced EPR bills in 2025 and ALL4 will continue to follow any updates that occur throughout 2026.

It is crucial to develop a robust data management framework for these EPR rules, as they will soon carry associated fees. This helps ensure your company does not pay more than necessary.

5. STRATEGIC Recommendations for 2026