Colorado to Issue New General Permit for Stormwater Discharges Associated with Non-extractive Industrial Activity

The Colorado Department of Public Health and Environment’s (CDPHE) Discharge Permit System (CDPS) has issued Draft General Permit COR900000 for Stormwater Discharges Associated with Non-extractive Industrial Activity (permit). The permit is currently in a public comment period that is set to end on June 13, 2022. The last COR900000 permit’s expiration date was June 30, 2017, but it was administratively extended.

The draft permit includes a few new topics. The first is lower benchmark monitoring concentrations for several parameters, mostly metals. Benchmark monitoring involves the sampling of stormwater runoff and is required for some industrial sectors. A facility’s sector is determined by its Standard Industrial Classification (SIC) code. The benchmark analytical data help characterize the quality of facility discharges and are compared to values listed in the permit to evaluate the effectiveness of storm water management controls.

Additional Implementation Measures (AIM) have also been added to the draft permit. These are basic control measures that must be implemented if certain trigger conditions are met (such as a benchmark monitoring exceedance or an unauthorized release or discharge). There are three AIM levels. A facility starts at baseline, and a trigger condition will cause the facility to proceed to AIM Level 1. A facility may return to baseline status if required control changes have been made and the average of the next four quarterly benchmark monitoring results for the contaminant-of-concern is below the benchmark concentration. A successive trigger condition will move the facility into the next AIM level. More stringent storm water management controls must be implemented at each higher AIM level.

The draft permit will not allow per- and polyfluoroalkyl substances (PFAS) in facility discharges. PFAS are chemicals used in fire-fighting foam (e.g., aqueous film forming foam, or AFFF), food packaging, carpet, and non-stick products. They can cause adverse health issues and are persistent in the environment. Benchmark monitoring for PFAS will be required for certain sectors (e.g., Sector S – Air Transportation, SIC code 45). Target concentrations have not been included, but in 2016 the United States Environmental Protection Agency (U.S. EPA) issued a health advisory level of 70 ng/L for the sum of perfluorooctanoic acid (PFOA) and perfluorooctanesulfonic acid (PFOS) in drinking water.

Another addition to the draft permit that has the potential to impact the regulated community involves coal tar. Areas where coal tar sealant has been applied (after the pending effective date of the permit) will not be eligible for permit coverage due to high levels of polycyclic aromatic hydrocarbons (PAH) associated with coal tar. Several PAH are known carcinogens. Coal tar sealant is typically used to coat asphalt surfaces. Existing coal tar coatings must be documented in a facility’s (required) annual reports. Alternatives could be to remove the coal tar or obtain a National Pollutant Discharge Elimination System Individual permit.

Once the permit is issued, those seeking coverage under it will have to apply via Colorado Environmental Online Services (CEOS). A facility must have a Stormwater Management Plan (SWMP) in place before applying. CDPHE normally mails existing permit holders a letter to inform them when it is time to re-apply. The typical time allowed for re-application is 90 days.

ALL4 is available to assist with your permitting or compliance needs. If you have questions about how the draft permit could affect your facility, please reach out to Adam Czaplinski at aczaplinski@all4inc.com.

Pennsylvania Department of Environmental Protection Releases New Draft Environmental Justice Policy

The Pennsylvania Department of Environmental Protection (PADEP or Department) Office of Environmental Justice (OEJ) released a draft revision to the state’s Environmental Justice (EJ) Policy on March 12, 2022 (Document Number 012-0501-002). The document was open for public comments through May 11, 2022.

The original policy was released in 2004, and there have been significant updates to the policy which broaden the scope of EJ initiatives and who is affected. The number of permits that could be subject to the policy has expanded and the Department has added more clarity and emphasis surrounding the public comment period. The following is a list of the main sections that have been added or revised:

- Addition of a “Definitions” section

- Addition of the responsibilities of the OEJ

- Revisions and clarity surrounding “Opt-in permits”

- Addition of oil and gas facility requirements

The proposed policy provides a list of definitions of commonly used words surrounding EJ, and a brief history and background regarding the state’s EJ policies. The Department defines an Environmental Justice Area as the geographic location where PADEP’s EJ Policy applies and specifies that the method to determine EJ Areas will be outlined in a separate document, which allows for the areas to be updated timely and accurately with the most recent EJ data. To determine if your facility is in an EJ Area, please visit the Department’s EJ Areas Viewer.

The responsibilities of the OEJ are outlined and expanded in Section I, Part C of the document. The OEJ serves as the liaison between PADEP, communities, and regulated entities. The OEJ is now responsible for developing and implementing an EJ training plan for PADEP staff; establishing an online repository of EJ information; reviewing and updating EJ maps on the OEJ website; issuing annual reports detailing the OEJ programs, results of trigger permit public participation, and grants and funding information; and developing strategic plans every five years.

The two types of permits covered in the policy, Trigger and Opt-in Permits, have remained unchanged; however, more clarity surrounding Opt-in Permits has been added. Trigger permits are identified as permits relating to activities that have traditionally led to public concern regarding the environment and human health. Opt-in permits are not listed in the criteria for Trigger permits but are evaluated on a case-by-case basis as determined by many factors including environmental impacts, community concerns, and cumulative impacts of the project. The following project facilities may obtain Opt-in Permits:

- Major sources of air pollution

- Resource recovery facilities or incinerators

- Sludge processing facilities, combustors, or incinerators

- Sewage treatment plants with capacities greater than 50 million gallons per day

- Transfer stations, solid waste facilities, or recycling facilities intending to receive 100 tons or more of recyclable materials per day

- Scrap metal facilities

- Landfills, including, but not limited to, facilities accepting ash, construction or demolition debris, or solid waste

- Medical waste incinerators

PADEP will evaluate Opt-in source category facilities on a case-by-case basis through assessing community concerns, environmental impacts, and cumulative impacts. The Department maintains the responsibility for determining which permits will be Opt-in Permits.

Finally, the proposed policy includes requirements for “unconventional” oil and gas facilities under Section IV of the document. The Department intends for operators to provide information regarding planned and ongoing activities to the communities, and for the communities to participate in decision making that affects the environment and economy. The requirements listed in this section of the policy will only apply to unconventional oil and gas well permits.

The last four sections of the document outline inspections, compliance, and enforcement; climate initiatives; community development and investments; and policy updates regarding the EJ Policy. The sections describe how the Department intends to prioritize EJ areas, and notes that the policy is subject to review by the DEP Secretary at least every four years to determine if any revisions are necessary.

The public comment period for the updated EJ Policy ended on May 11, 2022, with a final policy and the expected during the summer of 2022. For more information about the policy or EJ, please visit PADEP’s EJ Website.

Based on public hearings held by the Department, Facilities subject to EJ should expect more public participation throughout the permitting process and may be required to provide additional notifications to the community. EJ issues, perceived or real, will likely adversely impact permitting timelines for EJ-affected projects and Facilities should plan accordingly. Ultimately, the Trigger and Opt-in permitting review and determination will continue to be at the discretion of the Department. ALL4 will continue to monitor this policy and others as we update you on changing regulations. If you have any questions regarding EJ or permitting, please contact your Managing Consultant or info@all4inc.com.

WQC For PFOA and PFOS Out For Public Comment: What You Should Know

What’s being proposed?

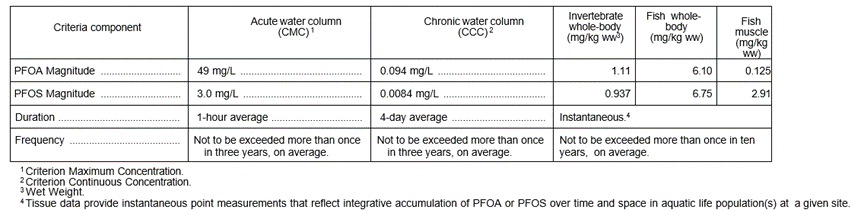

The United States Environmental Protection Agency (U.S. EPA) published the Draft Recommended Aquatic Life Ambient Water Quality Criteria (WQC) for Perfluorooctanoic Acid (PFOA) and Perfluorooctane Sulfonic Acid (PFOS) in the May 3, 2022 Federal Register (FR). The comment period for these WQC ends June 2, 2022. U.S. EPA is establishing recommended criteria based on best available science at the time of publication. Establishing aquatic life ambient WQC is one of the first steps, along with establishing maximum contaminant level (MCL) to regulating PFOA and PFOS under the National Pollutant Discharge Elimination System (NPDES) permits. Table 1 from the FR shows the recommended WQC.

TABLE 1—DRAFT RECOMMENDED FRESHWATER AQUATIC LIFE WATER QUALITY CRITERIA FOR PFOA AND PFOS

Why are U.S. EPA Recommendations for new WQC important?

WQC are established under Section 304(a)(1) of the Clean Water Act (CWA). The CWA directs U.S. EPA to develop and publish criteria reflecting the latest scientific data. The recommendations published by U.S. EPA are not regulations but are provided for authorized states and tribes to adopt. CWA Section 303(c)(1) requires states to review and modify, if appropriate, their water quality standards at least once every three years, which is known as the Triennial Review. Additional public comments will be taken during each state’s triennial review process.

Once a WQC is adopted by a state, those criteria are used to develop regulatory limits for NPDES permits and assess water bodies for impairments, with corresponding development of total maximum daily loads (TMDLs) for particular pollutants.

Water quality-based effluent limitations (WQBELs) may be incorporated into NPDES permits where a discharger’s effluent has the potential to cause the receiving stream to exceed the WQC for a given pollutant or where a TMDL has been established. For bioaccumulative compounds such as PFOA/PFOS, NPDES permits may contain both a short-term (e.g., daily) and long-term (e.g., annual) discharge limit. States may implement compliance schedules in NPDES permits to allow dischargers time to meet the new discharge limit and/or pollutant minimization plans (PMPs) for impaired waters (water bodies that do not meet the WQC).

How can my industry or company provide input into the process?

The timeline from Draft Recommended WQC to implementation of WQC as permit limits can be as long as 3 to 5 years depending on the Triennial Review schedule for your state and development of regulations once the WQC are adopted. States may have provisions for automatic updates to certain permits or may require those criteria to be added during permit modifications and renewals.

The first step is to establish whether the Draft WQC are applicable to your process. PFOA and PFOS have a wide range of uses and are used in many industries. If WCQ for PFOA and PFOS are applicable to you, there are many opportunities to provide comments. It is easier to influence potential changes to your compliance at the beginning of the process than at the end.

U.S. EPA is currently taking comments on the recommended WQC limits. Comments should consider the scientific data used to develop the criteria and how the criteria are applied. Once published as recommended WQC, the next opportunity to comment is during each state’s Triennial Review. Once a state adopts the WQC, input on how it is applied to your specific permit or water body is more difficult, but public comments are still taken during permits renewals, waterbody designations, and development of TMDLs.

ALL4 assists industry associations and companies with regulatory reviews and development of comments. If you are interested in learning more about our work or would like to discuss this or other water issues, please contact Karen Thompson at Kthompson@all4inc.com or Lizzie Smith at LSmith@all4inc.com.

Is this the “New Normal” for Procuring Monitoring Equipment?

Industrial facilities across the country are continuing to feel the impacts of the global pandemic, rising inflation, and supply chain disruptions. So how does this affect you and your ability to procure monitoring equipment? Unfortunately, the answer is that lead times are longer and costs have increased. We’ll dig into each of these to help your facility navigate the current challenges of monitoring equipment procurement.

Lead Times

Supply chain disruptions are causing monitoring equipment lead times to increase. The manufacturer and transport of parts and materials are taking longer than the pre-pandemic era. The lead times may be further extended for components made of exotic materials or electronic (or chip based) components that need to be shipped from overseas, especially those sourced in Asia. For example, equipment used to monitor the net heating value of vent gases, such as gas chromatographs, have lead times that have increased by more than 10 weeks when compared to the pre-pandemic world. It’s important to note that these lead times start once the purchase order has been issued, so it’s imperative to begin planning for your monitoring equipment needs early. Also, you may have to be flexible on specific design requirements for monitoring systems. Accept substitutions, it may be the only way to procure a complete monitoring system. Delays are not only limited to equipment; the resources needed to design, build, and integrate a monitoring system are also stressed.

Inflation

The current national inflation rate is over 8 percent; however, some monitoring equipment components are experiencing inflation rates higher than the national average. We are seeing monitoring equipment quotations with a validity of 30 days in the best case scenarios. In some situations, the quotations are only valid for 3 days. The validity of a quote is not only based on cost but also availability. What is in inventory today may not be in inventory tomorrow, and who knows when more inventory will be available. This means your facility needs to make decisions on monitoring equipment quickly to avoid a cost increase if a new quotation needs to be issued. One more thing: this isn’t a “throw more money at it” kind of thing. If the equipment is not available and can’t be obtained, money will not magically make the equipment appear.

Take Aways

As you can see, increasing lead times and inflation can both slow down implementation and increase the cost of monitoring equipment projects. It would be nice to able to quantify the number of weeks you should plan for or the dollars of increased cost; however, these factors are consistently changing to the point where ALL4 is not surprised at what we are seeing in quotations anymore. It seems to be the new normal and we have to react and plan for it the best we can. It is key to be in communication and collaboration with your suppliers. Make sure to communicate expectations clearly and often and set check in meetings along the way. Getting budgets approved will allow the team to issue purchase orders and get the equipment moving more quickly. Consider being flexible on your terms and conditions and approved manufacturers list. Line up your installation contractors early and be willing to install late items in the field when necessary. The bottom line is: don’t wait to begin planning for projects that require installation of monitoring equipment.

If you take action to mitigate the risk of monitoring equipment not being installed and operating by a specific compliance date, there may be room to request an extension. If a regulatory agency needs to be approached to consider an extension request, be prepared to show a “good faith effort” in procuring the equipment. Having clear documentation of the steps taken, including issuance of purchase orders, to procure the equipment and manpower to execute a project on time will be crucial for justifying the extension to the agency.

If you’re interested in how the current monitoring equipment procurement challenges impact your facility or project, please contact Katie Fritz at kfritz@all4inc.com or your ALL4 project manager for support.

Unpacking U.S. EPA’s Strategic Plan & Budget

The U.S. Environmental Protection Agency (U.S. EPA) published its Strategic Plan for Fiscal Year (FY) 2022-2026 on March 28, 2022. As described by U.S. EPA, “the Strategic Plan provides a roadmap to achieve EPA’s and the Biden-Harris Administration’s environmental priorities over the next four years.” Shortly after releasing the Strategic Plan, U.S. EPA released its justification for the FY 2023 Congressional Budget (Budget), in which the Biden Administration requested nearly $11.9 billion for U.S. EPA. I will not pretend to have read the nearly 1,400 pages of material comprising the Strategic Plan and Budget, but as one would expect, the requested Budget generally aligns with the goals of the Strategic Plan. Let’s explore each in a little more detail.

Strategic Plan

U.S. EPA released both a 5-page overview as well as the full 99-page Strategic Plan. The Strategic Plan begins by identifying the following four principles:

- Follow the Science

- Follow the Law

- Be Transparent

- Advance Justice and Equity

U.S. EPA states in its news release that the first three principles reflect a “renewed commitment to the three principles articulated by EPA’s first Administrator, William Ruckelshaus,” while the fourth principle of advancing justice and equity is new.

The Strategic Plan continues by outlining seven strategic goals. U.S. EPA states that “for the first time, EPA’s final Strategic Plan includes a new strategic goal focused solely on addressing climate change and an unprecedented goal to advance environmental justice and civil rights.” The seven strategic goals are as follows:

- Goal 1: Tackle the Climate Crisis

- Goal 2: Take Decisive Action to Advance Environmental Justice and Civil Rights

- Goal 3: Enforce Environmental Laws and Ensure Compliance

- Goal 4: Ensure Clean and Healthy Air for All Communities

- Goal 5: Ensure Clean and Safe Water for All Communities

- Goal 6: Safeguard and Revitalize Communities

- Goal 7: Ensure Safety of Chemicals for People and the Environment

Each of the seven goals has at least two objectives, and each objective has several Long-Term Performance Goals (LTPGs). Perhaps unsurprisingly, of the seven strategic goals, the goal pertaining to environmental justice and civil rights – relating directly to the new principle – leads in the number of LTPGs with 14. The goal pertaining to the safety of chemicals follows with 10 LTPGs. The observation that these two goals lead in LTPGs aligns with actions that U.S. EPA has already taken (more on that later).

We often hear that when setting goals, they should be measurable, and U.S. EPA applies that concept by establishing “a suite of measures that will help the Agency monitor progress and ensure accountability for achieving its priorities to protect human health and the environment for all Americans.” Of the 51 LTPGs in the Strategic Plan, 41 have numerical measures (e.g., percentages, quantities, dollars, etc.). For those LTPGs that do not appear to be as measurable, U.S. EPA footnotes in the Strategic Plan that the first-year activities will include further defining the scope of those goals.

A few examples of U.S. EPA’s LTPGs are to “conduct 55% of annual EPA inspections at facilities that affect communities with potential environmental justice concerns,” “increase the percentage of updated permits at RCRA facilities to 80% from the FY 2021 baseline of 72.7%,” and “complete at least eight High Priority Substance TSCA risk evaluations annually within statutory timelines compared to the FY 2020 baseline of one.”

The Strategic Plan goes on to present four cross-agency strategies to achieve the plan’s goals:

- Ensure Scientific Integrity and Science-Based Decision Making

- Consider the Health of Children at All Life Stages and Other Vulnerable Populations

- Advance EPA’s Organizational Excellence and Workforce Equity

- Strengthen Tribal, State, and Local Partnerships and Enhance Engagement

Most of these strategies also have measurable metrics, and clearly align with the previously stated principles and goals.

Finally, the Strategic Plan presents three U.S. EPA Priority Goals:

- Phase down the production and consumption of hydrofluorocarbons (HFCs)

- Deliver tools and metrics for EPA and its Tribal, state, local, and community partners to advance environmental justice and external civil rights compliance

- Clean up contaminated sites and invest in water infrastructure to enhance the livability and economic vitality of overburdened and underserved communities

These priority goals also align with the stated principles, goals, and strategies – particularly pertaining to climate change, environmental justice and civil rights, and water and chemical safety – and similarly align with the aforementioned actions U.S. EPA has already taken that I promised to discuss later.

Budget

U.S. EPA states in its news release that “the Budget makes historic investments to advance key priorities in the FY 2022-2026 EPA Strategic Plan, including tackling the climate crisis, advancing environmental justice, protecting air quality, upgrading the Nation’s aging water infrastructure, and rebuilding core functions at the Agency.” The requested FY 2023 budget ($11,880,841) represents nearly a 30% increase over FY 2022 ($9,237,153). The following priorities are listed:

- Upgrading Drinking Water and Wastewater Infrastructure Nationwide

- Ensuring Clean and Healthy Air for All Communities

- Tackling the Climate Crisis

- Advancing Environmental Justice

- Protecting Communities from Hazardous Waste and Environmental Damage

- Strengthening our Commitment and Ability to Successfully Implement Toxic Substances and Control Act (TSCA)

- Tackling Per- and Polyfluoroalkyl Substances (PFAS) Pollution

- Enforcing and Assuring Compliance with the Nation’s Environmental Laws

- Restoring Critical Capacity to Carry Out EPA’s Core Mission

Most of these nine priorities directly align with the seven goals of the Strategic Plan, with PFAS applying to both the air and water goals. (Interestingly, PFAS are not specifically mentioned in the Strategic Plan overview, only in the full plan.) The priority of restoring U.S. EPA’s capacity is an overarching priority needed to achieve the others.

As with the Strategic Plan, U.S. EPA released both a summary – 90-page Budget in Brief (BIB) – and the full 1,205-page Fiscal Year 2023 Justification of Appropriation Estimates for the Committee on Appropriations. While the Budget priorities align with the Strategic Plan goals, the order or the goals changes when listed from highest to lowest monetary investments:

| Strategic Plan Goal | FY 2023 Budget |

| Goal 5: Ensure Clean and Safe Water for All Communities | $6.2 billion |

| Goal 6: Safeguard and Revitalize Communities | $1.8 billion |

| Goal 4: Ensure Clean and Healthy Air for All Communities | $1.1 billion |

| Goal 3: Enforce Environmental Laws and Ensure Compliance | $852 million |

| Goal 1: Tackle the Climate Crisis | $773 million |

| Goal 2: Take Decisive Action to Advance Environmental Justice and Civil Rights | $615 million |

| Goal 7: Ensure Safety of Chemicals for People and the Environment | $517 million |

| Total | $11.9 billion |

There may be a few reasons for these differences. First, not all goals require the same amount of investment to be achieved. For example, upgrading water infrastructure clearly requires a significant investment for planning, materials, labor, construction, etc. Additionally, recall that the budget is only for FY 2023 while the Strategic Plan is for FY 2022-2026, so other goals may receive additional funding in future years.

Results

U.S. EPA’s Strategic Plan and Budget are thorough and organized, and contain a significant number of goals, priorities, and strategies, with many (mostly) measurable metrics. U.S. EPA states these “will help the Agency monitor progress and ensure accountability for achieving its priorities to protect human health and the environment for all Americans.” Results will be published on U.S. EPA’s Planning, Budget, and Results page. As of the time of this blogpost, the FY 2021 Agency Financial Report is available, with additional data “coming soon.”

However, since the Strategic Plan was released (and even prior to that), U.S. EPA has already taken actions that align with the plan’s goals. A few notable actions are provided below:

- On February 18, U.S. EPA released a new version of EJSCREEN. On the same day, the White House Council on Environmental Quality (CEQ) released a new tool called the Climate and Economic Justice Screening Tool (CEJST). You can read more about these tools here.

- On April 5, U.S. EPA proposed to ban the use of asbestos under TSCA.

- On April 14, U.S. EPA released its Equity Action Plan, which identifies six priority actions of its own. You can read more about that here.

- On April 19, U.S. EPA released an update on their progress on implementing the American Innovation and Manufacturing (AIM) Act, which pertains to a phased reduction of the use, manufacture, and import of hydrofluorocarbons (HFCs).

- On April 21, U.S. EPA released a White Paper on Reducing Climate Pollution from New Gas-Fired Turbines.

- On April 28, U.S. EPA announced three actions pertaining to their 2021-2024 PFAS Strategic Roadmap; specifically, “by improving methods to detect PFAS in water, reducing PFAS discharges into our nation’s waters, and protecting fish and aquatic ecosystems from PFAS.”

It’s nearly impossible not to hear something in the news almost daily about environmental justice, climate change, infrastructure, or other environmental issues. It’s no coincidence that U.S. EPA’s Strategic Plan and Budget align with those concerns and it’s clear that U.S. EPA is actively and continuously taking steps to execute the goals of the Strategic Plan. While it may take me through FY 2023 to read all of the material, I expect many more actions will have taken place by that time.

As public interest grows stronger and U.S. EPA focuses their resources on addressing public concerns, the regulated community must also ensure they are prepared to transparently communicate with public stakeholders, in addition to maintaining ongoing compliance with Federal, state, and local regulations. Having a communication strategy in place and digital tools to manage and present environmental data are becoming more and more necessary to keep up with public expectations. Please feel free to contact me at 610.422.1122 or lkroos@all4inc.com if you have any questions about the FY 2022-2026 Strategic Plan or FY 2023 Congressional Budget and how U.S. EPA’s goals and priorities may impact your facility.

A Quick Dive into Proposed Clean Water Act Hazardous Substance Worst Case Discharge Planning Regulations

On March 28, 2022 the U.S. Environmental Protection Agency (U.S. EPA) proposed a new rule, expanding on the current regulations at 40 CFR §118, as authorized under the Clean Water Act (CWA). The proposed rule would require all non-transportation related, onshore facilities to prepare and submit a Facility Response Plan (FRP) addressing the potential worst-case discharge of hazardous substances with the potential to cause substantial harm to the environment. The current rule only covers potential discharges of oil. This proposed rule could impact many industries and manufacturers.

Facilities with an onsite maximum capacity of a CWA hazardous chemical above 10,000 times the reportable quantity (RQ), as identified in 40 CFR §117.3, and located within one-half mile of navigable waters or conveyances to navigable waters will need to evaluate the following criteria to determine if the facility will be subject to the proposed rule.

- Past RQ releases to water,

- Modeled worst case discharges to fish, wildlife, and sensitive environments (FWSE),

- Modeled worst case discharges to public water systems, and

- Modeled worst case discharges to public receptors.

Navigable waters of the United States (navigable waters) as used in sections 311 and 312 of the Federal Water Pollution Control Act are:

- Territorial seas of the United States,

- Internal waters of the United States that are subject to tidal influence,

- Internal waters of the United States that are subject to tidal influence that are or have been waterways for transportation or been improved to connect waters, and

- All waters with the United States that are tributaries to such waters.

The U.S. EPA Regional Administrator will also be authorized to require that facilities prepare and submit a FRP regardless of the criteria noted above.

If subject to the rule, a facility must develop, implement, and submit an FRP. Plans are comprised of multiple requirements including:

- Identification of Qualified Individuals,

- Identification of key response resources,

- Routine employee training and response drills,

- Risk identification and characterization,

- Communication plans with Local Emergency Planning Committees (LEPC), and

- Release detection.

What do I need to do?

Upon final issuance of the rule, facilities will need to determine the applicability to their facility based on specific criteria within the rule and, if, submit a FRP within 12 months after the effective date of the final rule. It is worth noting that the comment period on the proposed rule will close on July 26, 2022. It could be several months until the final rulemaking is published.

If you have questions about how the proposed CWA rule could affect your facility’s compliance, or what your next steps should be once the rule is finalized, please reach out to Matt Dabrowski at mdabrowski@all4inc.com or Karen Thompson at kthompson@all4inc.com. ALL4 is monitoring all updates published by the U.S. EPA on this topic, and we are here to answer your questions and assist your facility with any aspects of facility response plan compliance.

Advantages of a Digital Solutions Tool Over Spreadsheets

Software is continuously evolving; however, many organizations tend to maintain vast numbers of spreadsheets. Spreadsheets are a useful tool for compiling and working with data but there are better options. The use of spreadsheets can ultimately lead to loss of time and revenue for an organization. Environmental Health and Safety (EHS) compliance processes can be especially intensive, with complex data relationships and calculations. Often organizations may not realize the variety of Digital Solutions tools that are available. These tools can be selected based on specific compliance processes and best fit for organizational structure. They can ultimately better equip an organization to manage their compliance processes and data.

Transparency

Spreadsheets are easily accessible to users; however they may not always be easily visible to stakeholders. It may take a lot of effort and time for a user to prepare a spreadsheet, and while the spreadsheet is highly malleable, it can be difficult for other users to interpret the work and make use of the data. If records are not easily produced, it may be difficult to show regulatory agencies evidence of compliance with EHS requirements. Additional ways a Digital Solutions tool can increase transparency include:

- Information can be more visible to others, including those at the corporate level.

- Tools may include a centralized data storage location.

- Many business intelligence tools (such as Power BI or Tableau) can pull data directly from Digital Solutions tools, providing real-time access and enhanced visualization of the data being collected.

- Many Digital Solutions tools also incorporate visual reporting or dashboarding within the tool.

- Collaboration can be done safely and consistently, preventing the creation of multiple versions and inconsistencies in the data.

Consistency

In many cases the existing compliance system is site or person specific, with cross-site issues arising. If sites or people across a company all operate with unique systems or practices in spreadsheets, it can be difficult to combine, compare, and report on that data. Digital Solutions tools can provide consistency in data and organizational structure to an EHS compliance system. Ways a Digital Solutions tool can increase consistency include:

- Organizational structure can allow the information to be rolled up into useful, reportable units.

- If someone leaves or changes roles in an organization, a Digital Solutions tool can provide a smoother transfer of knowledge than a spreadsheet.

- A Digital Solutions tool can be scaled with the organization as it grows.

- A Digital Solutions tool can help facilitate best practices across sites for compliance tasks, inspection checklists, and other compliance requirements.

- Because the data are in the same units and format, a Digital Solutions tool can make it easier to compare performance and/or results across multiple sites and identify areas for further analysis or improvement.

Ease of Use

Complex spreadsheets can be difficult to use efficiently. Multiple tabs and complex linking formulas can make it difficult to navigate the information. Spreadsheets can be time-consuming, with many complex functionalities requiring high-level experience. Complex emissions calculations can be especially intensive. Ways a Digital Solutions tool can be easier to use include:

- Records in a Digital Solutions tool are kept in one place, which can make data easier to find and allow users to easily respond to record requests.

- Digital Solutions tools provide user-friendly Graphical User Interfaces (GUI) that are simple to learn and provide a quick and efficient way to work in the system.

- A Digital Solutions tool can also be efficiently incorporated with other systems across the business.

- Automated workflows in a Digital Solutions tool can be an effective way to streamline the work processes of the organization.

- In a Digital Solutions tool the use of templates for complex emissions calculations can be created and reviewed once and then reused as often as the calculation methodology applies.

- Digital Solutions tools can make it easier to quality assure information by making it harder for the user to make an error, input bad data, delete something, or mistakenly change a calculation.

Data

The most important aspect of transitioning from the use of spreadsheets to using a Digital Solutions tool is the data. Simple and smart data structures in a database are safer to use. The data is less likely to be lost or corrupted. Data can also be more readily gathered and compiled to produce reports and dashboards. These reports can be vital in identifying trends, which can then be used to inform business decisions that can improve organizational processes. Ways a Digital Solutions tool can improve data include:

- Data relationships within the system can help users access and use data across different parts of the tool.

- Data relationships can also provide useful hierarchies for the data.

- Audit trails can allow users to easily view changes to data in the system.

- The data can be communicated to other digital tools in the company.

- Data are standardized to the same units and format.

- Finding data sets is easier because formal queries can be used on the data structures.

- Data can be analyzed to develop proactive, rather than reactive, responses and strategies based on trends. For example, safety data could identify similar causes behind near miss safety incidents. Environmental data might enable an organization to see when they are approaching an emission or operational limit before the limit is reached.

Security

Security is an important consideration. People within an organization may have different security levels. Access levels can be designated in a Digital Solutions tool so that users may be able to see their business area or geographic area only, whereas spreadsheet security is usually limited, and a spreadsheet can be e-mailed to anyone or easily deleted or modified, whether intentionally or unintentionally. Many Digital Solutions tools can also incorporate Single-Sign-On (SSO) and/or Multi-Factor Authentication (MFA) to better protect from unauthorized use.

Conclusion

Spreadsheets continue to have a place in some applications, but for many business processes a Digital Solutions tool may help organizations work smarter and more efficiently. By selecting a Digital Solutions tool that is appropriate for organizational size and processes, the transition away from spreadsheets can be less burdensome and can provide a lot of value. These tools can allow more transparency to key stakeholders. They can also provide additional consistency in data use and compliance processes for an organization. User-friendly interfaces can make the tool much simpler and easier to use. Simpler and smarter data opens the door to better data analysis and visualization. Security can also be improved, protecting the organization. Complexity in compliance processes can become a thing of the past, with organizations having easier, more transparent, and consistent compliance tools.

ALL4’s Digital Solutions Practice has extensive experience helping client’s scope, select, implement, maintain, and upgrade various types of digital tools. If you would like to discuss a digital solution for your company, please contact Noah Zetocha at nzetocha@all4inc.com or 402-853-2538.

Ozone Nonattainment: Impact to Air Permitting

Under the Clean Air Act (CAA), the U.S. Environmental Protection Agency (U.S. EPA) sets National Ambient Air Quality Standards (NAAQS) for pollutants considered harmful to public health and the environment. A geographical area (which can vary from a partial county to multiple counties) that does not meet a NAAQS is classified as a nonattainment area.

U.S. EPA set the 2008 ozone standard to 75 parts per billion (ppb) and required all areas of the country to meet this monitored concentration by July 20, 2018. The areas that were not able to demonstrate compliance with this standard have now been classified as an ozone nonattainment area. U.S. EPA revised the standard to 70 ppb in 2015 but some areas have still not met the 2008 standard and their attainment status is about to change in level of severity.

Serious to Severe Nonattainment

On April 13, 2022, the EPA issued a proposed rule that would change the nonattainment status for six areas. The six areas listed below are currently classified as serious nonattainment areas and failed to meet the 2008 ozone NAAQS by the attainment date. U.S. EPA now proposes to reclassify these areas as severe nonattainment areas. Each area listed will have until July 20, 2027, to demonstrate compliance.

- Chicago-Naperville, IL-IN-WI

- Dallas-Fort Worth, TX

- Denver-Boulder-Greeley-Ft. Collins-Loveland, CO

- Houston-Galveston-Brazoria, TX

- Morongo Band of Mission Indians

- New York-N. New Jersey-Long Island, CT-NJ-NY

Impact to Air Permitting

The nonattainment classification has a direct impact on state air permitting programs and compliance for each facility in the areas noted above. Under the CAA, the major source threshold for a facility located in a serious nonattainment area is 50 tons per year for Nitrogen Oxides (NOx) and Volatile Organic Compounds (VOC). However, the major source threshold in a severe nonattainment area is 25 tons per year for NOx and VOC. Therefore, any facility located within the severe nonattainment area with the potential to emit greater than 25 tons per year of NOx or VOC will be required to obtain a Title V operating permit. Any new facility with potential emissions greater than or equal to 25 tons per year of NOx or VOC or any modification with an increase greater than or equal to 25 tons per year of NOx or VOC will have to go through nonattainment New Source Review (NSR). For such facilities that would be new to a Title V operating permit, compliance activities will become more rigorous with respect to recordkeeping and reporting requirements.

Another area that will need to be carefully examined would be emissions netting for new projects at an existing Title V facility. If your facility will be amending an existing NSR permit or starting a new NSR project, the trigger for netting will be reduced and the ratio for emissions offsets will become less favorable. Currently for serious nonattainment areas, the offset ratio is 1.2 to 1 and with a severe nonattainment classification, that will be changed to 1.3 to 1. In other terms, the emissions offset ratio is the ratio of total actual reductions of emissions to total emissions increases of such pollutants. For example, a 1-ton NOx increase would have to be offset with a 1.3-ton NOx decrease in a severe nonattainment area. With more stringent offset ratios permitting activities will become more difficult on the regulated community.

Summary

Deadlines for facilities to apply for a first-time Title V permit will be established following issuance of the final rule. The reclassification will be in place upon the effective date of the final rule and will impact any permit applications that are still being processed for facilities in the areas being reclassified. If your facility has a potential to emit greater than 25 tons per year of NOx or VOC, you may be subject to additional permitting requirements. ALL4 has the expertise to help navigate any new air regulatory requirements that may affect you and your facility. If you have any questions regarding this proposed rule and its impacts, please contact your ALL4 project manager or contact us at info@all4inc.com.

Will Agencies Regulate Air Emissions from Pyrolysis and Gasification Units Like they Regulate Air Emissions from Combustion Units?

Most people are familiar with combustion in some form or another. Whether it’s a campfire used to roast marshmallows, the oil burner used to heat your house on a cold winter day, or the engine that powers your car, combustion directly affects our lives on a daily basis. Many people, however, are not familiar with combustion cousins: pyrolysis and gasification.

As we continue to see a push for increased sustainability and a desire to extend the usefulness of materials, we have also seen an increase in the use of pyrolysis and gasification across many industrial sectors. Pyrolysis and gasification can be used to convert used plastics, biosolids, municipal solid waste, coal, and wood into fuels or feedstock for industrial chemical and consumer products manufacturing. The term “Advanced Recycling” has been applied to the conversion of waste materials into usable feedstock for industrial manufacturing; however, several states and industry associations oppose the application of the term “recycling” to these processes, instead preferring terms such as “thermomechanical conversion.” The use of these technologies to produce alternative fuels is also of interest as industry looks to reduce its use of traditional fossil fuels.

Key Terms

Congress did not anticipate the use of these technologies for waste treatment, so they did not define the terms pyrolysis and gasification in the Clean Air Act (CAA). However, they do appear in some of the regulations promulgated under CAA section 129 pertaining to solid waste combustion. Therefore, it is important to understand the definitions of the following terms:

Combustion1 – “The production of heat and light energy through a chemical process, usually oxidation. Products of complete combustion include water and carbon dioxide, while incomplete combustion can yield partially oxidized organic compounds and carbon monoxide. Factors that promote complete combustion include the proper fuel-air ratio, temperature range, and adequate amount of time for the fuel and its by-products to complete the combustion reactions.”

Pyrolysis2 – “Thermally decomposes or rearranges materials under process conditions where extremely little to no oxygen is present.”

Gasification3– Process that “converts feed materials (primarily carbonaceous) into syngas (carbon monoxide and hydrogen) and carbon dioxide. The materials are gasified when they react with controlled amounts of oxygen or steam at high temperatures.”

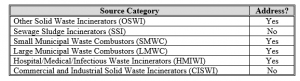

The following table summarizes which CAA section 129 regulations address pyrolysis and gasification:

Advanced Notice of Proposed Rulemaking

Due to the inconsistency in how pyrolysis and gasification are addressed in CAA section 129 regulations and the number of inquiries received on how to regulate air emissions from new pyrolysis and gasification units, on September 8, 2021, the United States Environmental Protection Agency (U.S. EPA) published an Advance Notice of Proposed Rulemaking (ANPR) to solicit information and comments to assist in the development of regulations for pyrolysis and gasification units. The notice received significant attention, resulting in an extension of the comment period from November 8 to December 23, 2021. Over 170 comments were received. It will be interesting to see how the comments are considered and whether a proposed regulatory action results from the review of the comments, given all U.S. EPA’s other competing priorities and goals and the disparate views on whether pyrolysis and gasification units should be regulated as waste incinerators or whether the process should be considered recycling. Some commenters asserted that regulating pyrolysis and gasification units under existing waste incinerator rules would stifle innovation and development of these technologies.

CAA Section 114 Request

In the ANPR, U.S. EPA indicated they are considering two potential pathways to regulate pyrolysis and gasification units, and published a draft questionnaire intended to collect data to determine the most appropriate way to regulate theses sources4. The data collected will be used by U.S. EPA in deciding whether to regulate these sources under CAA section 129 or as specific source categories under CAA section 111 and 112. CAA section 129 directs U.S. EPA to regulate solid waste incinerators. CAA section 111 is the underlying statute for the Standards of Performance for New Stationary Sources (NSPS) and CAA section 112 is the underlying statute for the 40 CFR Part 63 National Emissions Standards for Hazardous Air Pollutants (NESHAP). Regulations promulgated under CAA section 129 are generally more stringent than regulations promulgated under CAA sections 111 and 112.

State Level Regulatory Action

In addition to potential regulatory action related to air emissions from pyrolysis and gasification at the federal level, states may regulate these processes differently. For example, the Kentucky General Assembly recently approved an amendment to Kentucky Revised Statute (KRS) 224.1-010 to define Advanced Recycling as “a manufacturing process for the conversion of post-use polymers and recovered feedstocks into basic hydrocarbon raw materials, feedstocks, chemicals, and other products through processes that include pyrolysis, gasification, depolymerization, catalytic cracking, reforming, hydrogenation, solvolysis, and other similar technologies.” Under the proposed legislation, advanced recycling activities would be excluded from definitions related to solid waste, including, but not limited to “disposal” and “municipal solid waste disposal facility.” According to the American Chemistry Council, Kentucky is the 18th state to pass such an advanced recycling law, designating these types of facilities as manufacturers not waste incinerators.

Takeaways

As more units are being constructed, we are starting to see a significantly growing interest in regulating air emissions from pyrolysis and gasification units at both the state and federal level. If your facility is using pyrolysis or gasification in your process, you should anticipate agency proposals for additional regulations or amendments to existing regulations. ALL4 can assist you with determining how your state regulates these processes and what federal regulations might apply.

Completing a Section 114 request is outside the routine responsibilities of a facility’s environmental professional. If you are preparing for and completing a Section 114 Request, it can involve a significant commitment of time and resources. While the Section 114 Request is not final, it is not too early to begin preparations for developing a response.

ALL4 has extensive experience in assisting regulated entities navigate the complex web of state and federal environmental regulations and is keeping a close eye on developments related to pyrolysis and gasification. We will continue to monitor new federal and state regulations are they are developed. ALL4 has also assisted clients with data gathering and compilation and electronic submittals of information to U.S. EPA. If you have questions or require assistance with your project, please reach out to me at mmchale@all4inc.com.

1U.S. EPA. Basic Concepts in Environmental Sciences Glossary. U.S. EPA. [Online] January 29, 2010.

2 U.S. EPA. Draft Survey for Pyrolysis and Gasification Units. Docket Number EPA-HQ-OAR-2021-0382.

3 Id.

4The information U.S. EPA is proposing to request as part of the Section 114 request includes, but is not limited to the following:

- Construction and startup dates

- Description of the configuration

- Air emissions data from the pyrolysis and gasification chamber and downstream combustion devices.

- Purpose of the technology

A Closer Look at the SEC’s Proposed Climate Related Disclosure Rule

On March 21, 2022, the U.S. Securities and Exchange Commission (SEC) proposed new rules that would require publicly traded companies to disclose climate-related risks in annual reports and public filings, such as Form 10-K reports. The approximately 500-page draft rule and a fact sheet are available from the SEC website at https://www.sec.gov/news/press-release/2022-46.

The rule is currently open to public comment, with the deadline for comments being extended until June 17, 2022. The comment period was extended from May 20, 2022, after 21 States Attorneys General, the U.S Chamber of Commerce, and numerous trade and industry associations requested an extension. The SEC is planning to finalize the rule by the end of the year. However, as of this week, SEC has already received over 8,100 comments and many more are expected before the end of the comment period.

The proposed rule would require companies to report climate-related risks that are reasonably likely to have a material impact on their business, results of operations, or financial condition. Climate-related metrics, including greenhouse gas (GHG) emissions, would be required in a note to audited financial statements. More specifically, the proposed rules would require public companies to disclose information including:

- The oversight and governance of climate-related risks by the board and management.

- How any climate-related risks identified have had, or are likely to have, a material impact on the business and consolidated financial statements, which may manifest over the short-, medium-, or long-term.

- How any identified climate-related risks have affected, or are likely to affect, strategy, business model, and outlook for the company.

- Processes for identifying, assessing, and managing climate-related risks, and whether such processes are integrated into the overall risk management system or processes for the company.

- If the company has adopted a transition plan as part of its climate-related risk management strategy, a description of the plan, including the relevant metrics and targets used to identify and manage any physical and transition risks.

- If the company uses scenario analysis to assess the resilience of its business strategy to climate-related risks, a description of the scenarios used, as well as the parameters, assumptions, analytical choices, and projected principal financial impacts.

- If the company uses an internal carbon price, information about the price and how it is set.

- The impact of climate-related events (e.g., severe weather events, other natural conditions, and physical risks) and transition activities (including transition risks) on financial statement line items, and disclosure of financial estimates and assumptions impacted by climate-related events and transition activities.

- Scopes 1 and 2 GHG emissions metrics, separately disclosed, expressed both by constituent greenhouse gases and in the aggregate, and in absolute and intensity terms. In some cases, companies must obtain an attestation report (i.e., verification) from an independent attestation service provider covering, at a minimum, Scopes 1 and 2 emissions disclosure.

- Scope 3 GHG emissions and intensity, if material, or if the company has a GHG emissions reduction target or goal that includes its Scope 3 emissions.

- Any climate-related targets or goals, including:

- The scope of activities and emissions included in the target, the time by which the target is intended to be achieved, and any interim targets;

- How the company intends to meet its climate-related targets or goals;

- Relevant data to indicate whether the company is making progress toward meeting the target or goal and how progress has been achieved, with updates each fiscal year; and

- If carbon offsets or renewable energy certificates (“RECs”) have been used as part of the plan to achieve climate-related targets or goals, certain information about the carbon offsets or RECs, including the amount of carbon reduction represented by the offsets or the amount of generated renewable energy represented by the RECs.

When responding to any of the proposed rules’ provisions concerning governance, strategy, and risk management, companies may also disclose information concerning any identified climate-related opportunities.

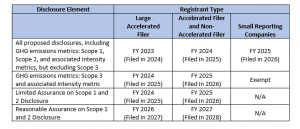

Reporting Phase-in Schedule

The proposed rules would be phased in over time, with an additional phase-in period for Scope 3 emissions disclosures and the assurance requirements. If the proposed rules are adopted with an effective date in December 2022, a company with a December 31st fiscal year-end would report as follows:

Toward Universal Climate Accounting Standards

The SEC’s proposed rule aligns closely with many of the Task Force on Climate-Related Financial Disclosures (TCFD) recommendations. Most of the TCFD’s requirements for disclosure of Scope 1, 2, and 3 emissions and the focus on climate governance, strategy, and risk management are reflected in the proposed SEC regulation. The proposal also requires companies to report these climate-related risks if they are likely to have material impacts on the business over short-, medium-, and long-term periods, similar to the TCFD’s strategy disclosure recommendations.

Last November, the International Financial Reporting Standards (IFRS) Foundation, a global organization that oversees financial accounting standards in more than 140 countries, including Canada, the United Kingdom, and the European Union, founded the International Sustainability Standards Board (ISSB). Following release of the SEC proposed rule, the ISSB released a first draft of its general sustainability-related and climate-related disclosure standards on March 31, 2022. While the details of the ISSB draft disclosure standards will be the subject of a future 4 The Record article, it can be said that these draft standards also closely follow the guidance of the TCFD recommendations.

Since the IFRS governs financial reporting in capital markets in more than 140 countries, and the SEC governs U.S. capital markets, which are the largest and deepest in the world, the SEC and ISSB would ideally collaborate closely in the development of the final rules and standards. Just as we need universal financial accounting standards, we also need universal climate accounting standards.

ALL4 will continue to monitor development of the SEC climate related disclosure rule and the ISSB disclosure standards as they develop. If you have questions regarding these proposals, reach out to one of our team members – Daryl Whitt at dwhitt@all4inc.com or Connie Prostko-Bell at cprostko-bell@all4inc.com.